Bangladesh Defense

Bangladesh DefenseSaif

Senior Member

- Jan 24, 2024

- 20,358

- 9,555

- Nation

- Residence

- Axis Group

$7b pledged in foreign funds

When Bangladesh is facing a reserve squeeze, it has received fresh commitments for $7.2 billion in loans from global lenders in the first seven months of fiscal 2023-24, a fourfold increase from a year earlier.

$7b pledged in foreign funds

24 projects to be implemented in health, education, transport, energy; fund commitment may cross $10b this fiscal year

When Bangladesh is facing a reserve squeeze, it has received fresh commitments for $7.2 billion in loans from global lenders in the first seven months of fiscal 2023-24, a fourfold increase from a year earlier.

That means the new commitments crossed the foreign loan target of $6 billion for this fiscal year.

When Bangladesh is facing a reserve squeeze, it has received fresh commitments for $7.2 billion in loans from global lenders in the first seven months of fiscal 2023-24, a fourfold increase from a year earlier.

That means the new commitments crossed the foreign loan target of $6 billion for this fiscal year.

Finance ministry officials hoped that the fund commitments would exceed $10 billion this fiscal year and provide some cushion to the economy, subject to quick utilisation.

The utilisation of the funds remains a cause for concern as Bangladesh could use only $4.4 billion in seven months against a target of $11.24 billion for this fiscal year.

To achieve the target, the government would have to spend $6.84 billion over five months, which could be difficult,given its poor record of timely project implementation.

Unused foreign funds stood at $47 billion as of January this year. It was $43.76 billion on June 30 last year, according to the finance ministry documents.

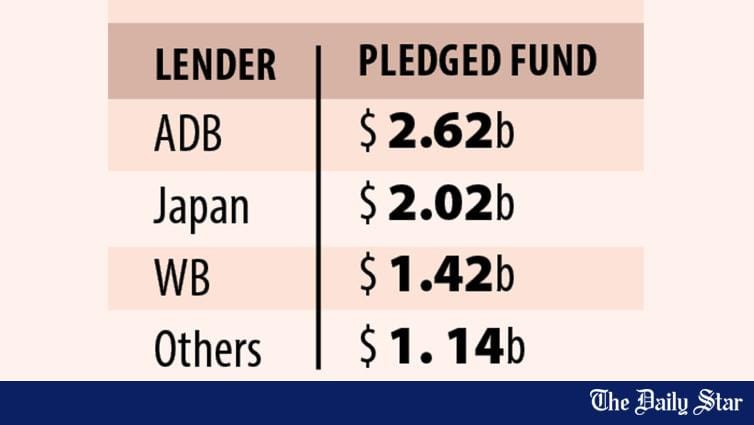

Of the $7.2 billion committed, the highest $2.62 billion was committed by the Asian Development Bank (ADB), followed by Japan $2.02 billion and the World Bank $1.42 billion. The rest $1.14 billion fund commitment came from other lenders.

Between July and January of 2022-23, Bangladesh received commitments for just $1.76 billion in foreign loans.

FUND FOR PROJECTS

As per the fresh commitments, ADB will finance 10 projects in health, education, transport, and energy sectors and for the local government and the Chittagong Hill Tracts.

The ADB has offered to finance a $336.47 million project to establish an international standard laboratory for vaccine research and production of high-quality vaccines.

It will provide $300 million for implementing a project to improve sub-regional transport and trade and 190km of Dhaka-Northwest corridor.

The ADB will also provide $200 million for the "Smart Metering Energy Efficiency Improvement Project" to prevent the waste of natural gas at home.

It will give $100 million to three public universities and the University Grants Commission to create skilled manpower in the manufacturing sector and to create jobs in the industrial sector.

About $90 million will be given to the Local Government Division's project for safe water supply and waste management in Rangamati, Bandarban, and Lama municipalities.

The Local Government Division will also get $490 million for two projects to improve rural connectivity, urban governance, and infrastructure.

Japan's $2.02 billion will go to two ongoing projects. One is the 1,200-megawatt coal power plant at Matarbari. The other project is for building the third terminal of the Hazrat Shahjalal International Airport.

The World Bank will provide $300 million for the economic inclusion of the youth through support for skill development, employment, self-employment, and entrepreneurship.

SLOW IMPLEMENTATION

The authorities have utilised $4.4 billion of foreign funds between July and January this fiscal year.

Of the amount, the ADB disbursed $1.24 billion, Japan $884 million, the World Bank $763 million, Russia $588 million, China $361 million, and India $169 million. Other lenders disbursed the rest.

Shahriar Kader Siddiky, secretary to the Economic Relations Division, said disbursement of foreign funds depends on project implementation.

"We are working in a coordinated way with the relevant ministries, development partners and their headquarters to increase the utilisation of the committed funds. Disbursement is increasing gradually," he told reporters on Sunday after a meeting between Finance Minister Abul Hassan Mahmood Ali and visiting World Bank Managing Director Anna Bjerde.

An ERD official, seeking anonymity, said they have utilised more than $10 billion in foreign funds during each of the last two fiscal years. The official said they used to spend $7 billion a year before that.

Replying to a question, the official said they were expecting commitments for $3 billion to $4 billion more during the last five months of this fiscal year.

LOAN REPAYMENT TO RISE TOO

The government's foreign debt repayment saw a rise of 44.54 percent over the first seven months of this fiscal year.

The government repaid $1.85 billion, which was $1.28 billion during the same period in the last fiscal year.

The surge in disbursement of foreign loans and interest payments against them is pushing up the debt servicing requirement, the ERD official said.

The utilisation of the funds remains a cause for concern as Bangladesh could use only $4.4 billion in seven months against a target of $11.24 billion for this fiscal year.

To achieve the target, the government would have to spend $6.84 billion over five months, which could be difficult,given its poor record of timely project implementation.

Unused foreign funds stood at $47 billion as of January this year. It was $43.76 billion on June 30 last year, according to the finance ministry documents.

Of the $7.2 billion committed, the highest $2.62 billion was committed by the Asian Development Bank (ADB), followed by Japan $2.02 billion and the World Bank $1.42 billion. The rest $1.14 billion fund commitment came from other lenders.

Between July and January of 2022-23, Bangladesh received commitments for just $1.76 billion in foreign loans.

FUND FOR PROJECTS

As per the fresh commitments, ADB will finance 10 projects in health, education, transport, and energy sectors and for the local government and the Chittagong Hill Tracts.

The ADB has offered to finance a $336.47 million project to establish an international standard laboratory for vaccine research and production of high-quality vaccines.

It will provide $300 million for implementing a project to improve sub-regional transport and trade and 190km of Dhaka-Northwest corridor.

The ADB will also provide $200 million for the "Smart Metering Energy Efficiency Improvement Project" to prevent the waste of natural gas at home.

It will give $100 million to three public universities and the University Grants Commission to create skilled manpower in the manufacturing sector and to create jobs in the industrial sector.

About $90 million will be given to the Local Government Division's project for safe water supply and waste management in Rangamati, Bandarban, and Lama municipalities.

The Local Government Division will also get $490 million for two projects to improve rural connectivity, urban governance, and infrastructure.

Japan's $2.02 billion will go to two ongoing projects. One is the 1,200-megawatt coal power plant at Matarbari. The other project is for building the third terminal of the Hazrat Shahjalal International Airport.

The World Bank will provide $300 million for the economic inclusion of the youth through support for skill development, employment, self-employment, and entrepreneurship.

SLOW IMPLEMENTATION

The authorities have utilised $4.4 billion of foreign funds between July and January this fiscal year.

Of the amount, the ADB disbursed $1.24 billion, Japan $884 million, the World Bank $763 million, Russia $588 million, China $361 million, and India $169 million. Other lenders disbursed the rest.

Shahriar Kader Siddiky, secretary to the Economic Relations Division, said disbursement of foreign funds depends on project implementation.

"We are working in a coordinated way with the relevant ministries, development partners and their headquarters to increase the utilisation of the committed funds. Disbursement is increasing gradually," he told reporters on Sunday after a meeting between Finance Minister Abul Hassan Mahmood Ali and visiting World Bank Managing Director Anna Bjerde.

An ERD official, seeking anonymity, said they have utilised more than $10 billion in foreign funds during each of the last two fiscal years. The official said they used to spend $7 billion a year before that.

Replying to a question, the official said they were expecting commitments for $3 billion to $4 billion more during the last five months of this fiscal year.

LOAN REPAYMENT TO RISE TOO

The government's foreign debt repayment saw a rise of 44.54 percent over the first seven months of this fiscal year.

The government repaid $1.85 billion, which was $1.28 billion during the same period in the last fiscal year.

The surge in disbursement of foreign loans and interest payments against them is pushing up the debt servicing requirement, the ERD official said.