Bangladesh Defense

Bangladesh DefenseSaif

Senior Member

- Jan 24, 2024

- 20,382

- 9,555

- Nation

- Residence

- Axis Group

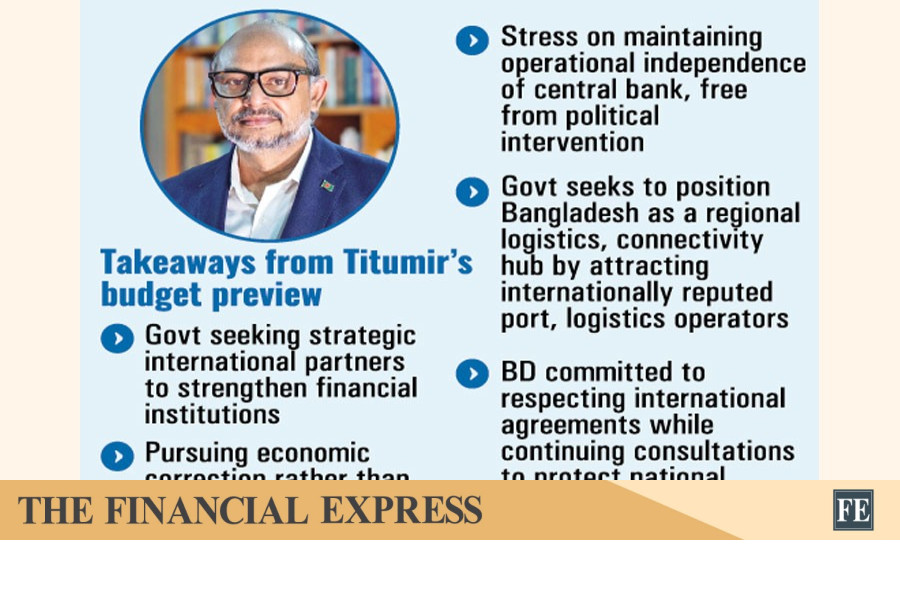

Can FY27 budget bring the economy back to life?

The budget, by all accounts, will be a large one

Can FY27 budget bring the economy back to life?

Md Asaduz Zaman

Highlights

Md Asaduz Zaman

Highlights

- Private sector credit growth hits historic lows

-

- GDP growth slows down to 3.03 percent

-

- NBR faces Tk 1.04 lakh crore shortfall

As Finance Minister Amir Khosru Mahmud Chowdhury prepares the FY27 budget, the central question is whether new fiscal measures can restore confidence among businesses amid mounting economic pressure.

But the timing could hardly be worse.

His first budget for the new government comes against an economic backdrop that leaves little room for optimism, let alone ambition.

Private investment has sunk to historic lows, industrial output is faltering, inflation refuses to yield, and the country’s debt obligations are quietly consuming a growing share of external receipts.

The budget, by all accounts, will be a large one. Whether the economy can bear it is another question entirely.

The most telling signal of the economy’s fragility lies not in headline growth figures, but in what businesses are actually doing, or rather, not doing. Private sector credit growth fell to 4.72 percent in March, a historic low that speaks to something deeper than a temporary slowdown.

When businesses stop borrowing, they stop investing, stop expanding and stop hiring, all of which contribute to unemployment. Over time, that reluctance becomes self-reinforcing.

The numbers bear this out.

Economic growth slowed to 3.03 percent in the October-December quarter of FY2025-26, down from 3.53 percent a year earlier.

The more alarming figure sits beneath that headline. The industrial sector, long the engine of Bangladesh’s growth model, slowed sharply to 1.27 percent from 5.78 percent a year earlier. That is not a slowdown but a near stall.

Before the new budget is even presented, the tax authority is already missing current targets. In the first ten months of FY2025-26, the National Board of Revenue (NBR) collected Tk 3.27 lakh crore, falling Tk 1.04 lakh crore short of its July-April target. That is not a marginal miss. It is a structural one.

To meet the target, the NBR would need to collect Tk 2.27 lakh crore in the remaining two months of the fiscal year. Officials themselves describe that prospect as a “herculean task” which is perhaps the most honest thing a revenue authority can say.

It signals not merely a bad stretch, but a fundamental mismatch between what the government expects to collect and what the economy is actually generating in tax receipts.

Faced with the shortfall, the government has turned increasingly to the banking system to finance its deficit, a shift that is beginning to affect private sector credit conditions.

In the July-February period of FY2025-26, net deficit financing rose 67 percent year-on-year to Tk 1.05 lakh crore, up from Tk 63,040 crore a year earlier. Of this, Tk 88,309 crore came from the banking system, according to Bangladesh Bank data.

When the government draws that heavily on the banking system, it competes directly with private borrowers for the same pool of credit. Banks, facing a captive and low-risk sovereign borrower, have less appetite and less capacity to lend to businesses.

The result is a crowding-out effect that is not theoretical; it is already showing up in the data.

Above all, persistently high inflation and a rapidly rising debt-servicing burden are squeezing the country’s fiscal space, leaving the government with less room to support growth, investment and jobs.

Business leaders and economists are clear-eyed about the risk.

Unless the government demonstrates genuine fiscal discipline, meaningfully expands the tax base, and takes visible steps to restore confidence in the investment climate, the budget’s revenue and growth targets will likely join a long line of lofty projections that quietly missed their marks.

That pattern of targets set, revised, and forgotten is precisely what erodes the business confidence the government now needs to rebuild.

Business Initiative Leading Development (BUILD) Chairperson Abul Kasem Khan has called for a shift away from “stereotypical” budget-making, urging realism, deregulation and broader reforms.

“We do not want a continuation of the stereotypical approach in the budget; rather we want novelty, modernisation, and genuine deregulation,” he said.

He questioned the feasibility of ambitious revenue targets in a slowing economy.

“If GDP growth has fallen from around 7 percent to nearly 3.5 percent, then expecting disproportionately high revenue collection raises serious questions,” he noted, adding that pressure on a narrow tax base could undermine compliance.

On the business environment, Khan stressed reducing the cost of doing business.

“As businessmen, what we want most is a reduction in the cost of doing business. That includes reforming advance income tax, addressing refund delays, and removing the back-and-forth policy approach that has long created uncertainty,” he said.

He also called for faster circulation of money and stronger consumption. “If we want the economy to function properly, we must allow money to circulate and consumption to grow. People’s purchasing power must increase so that they feel confident to spend, which in turn drives production and investment,” he added.

Khan further emphasised broad-based deregulation.

“Deregulation must be broad-based and meaningful. A small entrepreneur should be able to start a business within a day or two, without navigating months of licensing procedures,” he said, adding that implementation has lagged behind repeated reform promises.

Fazlul Hoque, former president of Bangladesh Knitwear Manufacturers and Exporters Association (BKMEA), said, “The government is still new, and we do not yet have a clear understanding of its performance capacity.”

“Perhaps it would have been better if the budget had been presented a little later, after fully assessing the economic realities.”

Hoque noted an “unwritten trend” of expanding budgets each year, driven partly by political considerations, and warned that weak revenues amid slowing activity could make targets difficult.

“When economic activities slow down, revenue earnings naturally decline. Imports fall, exports face difficulties and domestic consumption weakens,” he said, adding that large revenue gaps may force higher government borrowing and squeeze private credit.

“A large portion of government expenditure is now going toward interest payments on debt,” he said, stressing stronger fiscal discipline and reduced corruption.

“If corruption can be reduced, government income will rise while expenditure will fall at the same time,” he added.

The former BGMEA president also warned of inflationary pressure after the new pay scale for public employees and said weak fiscal management could hurt private sector credit and jobs.

“The government wants to create 1 crore jobs, but if the private sector suffers because of tighter credit conditions and higher interest rates, achieving that target will become difficult,” he said.

Kamran T Rahman, president of the Metropolitan Chamber of Commerce and Industry (MCCI), said relying on ambitious revenue targets without expanding the tax base is unsustainable.

“Putting additional pressure on existing taxpayers will only make the situation more difficult,” he said, noting that despite 1.28 crore TIN (taxpayer identification numbers) holders, only 40-45 lakh file returns, many of them zero returns.

He added that the NBR is often pushed to meet targets without broader reforms, while rising costs are already straining industries.

“If businesses cannot survive, then where will the taxes come from?”

Mahmud Hasan Khan, president of Bangladesh Garment Manufacturers and Exporters Association (BGMEA), also urged widening the tax net instead of increasing pressure on existing taxpayers, and stressed timely ADP implementation.

“A Tk 3 lakh crore ADP is a very big jump this time. But what usually happens is that after the announcement, midway through the year, the allocation gets cut back. That should not happen if they truly want implementation,” he said.

He cautioned that aggressive revenue pressure would hurt business sustainability in a fragile economy.

“In that context, increasing the revenue burden aggressively will not help businesses remain sustainable,” he said.

He stressed long-term policy consistency.

“Policies must be sustainable and long-term,” he said, noting ongoing discussions on policy predictability and prospective taxation up to 2030.