Bangladesh Defense

Bangladesh DefenseSaif

Senior Member

- Jan 24, 2024

- 20,382

- 9,555

- Nation

- Residence

- Axis Group

Can next budget meet enormous challenges?

A nation's budget for a particular financial year involves the government's comprehensive financial plan outlining its expected revenues and proposed expenditures for the next 12-month accounting period. Actually, the budget reflects the government's economic policies. From the outlines of th

Can next budget meet enormous challenges?

SYED FATTAHUL ALIM

Published :

Jun 07, 2026 23:01

Updated :

Jun 07, 2026 23:01

A nation's budget for a particular financial year involves the government's comprehensive financial plan outlining its expected revenues and proposed expenditures for the next 12-month accounting period. Actually, the budget reflects the government's economic policies. From the outlines of the proposed budget as provided by the government and discussed by experts, it is going to mark a shift from a debt-driven expansion to one that is focused on macroeconomic stabilisation, broad-based welfare and deregulation. The deregulation understandably involves reducing bureaucratic barriers and slashing the cost of business. Core measures would include separating customs into policy and implementation wings, extending duty-free bonded warehouse privileges to all exporters and establishing a single-point approval system for business licences and registrations.

Since the incumbent government inherited a fragile economy characterized by high inflation and declining private investment, the government's fiscal strategy aims to address these issues through several policy pillars. So, instead of the past practice of heavy central bank borrowing and printing money, the government, as part of investment-led growth, plans to promote domestic production by way of introducing a stimulus package of Tk 600 billion targeting agriculture, CMSMEs and export diversification. To control inflation and ensure social safety, the budget would expand social safety nets prioritising relief for low- and middle-income groups that includes a system of family cards and agricultural loan waivers. On the other hand, to manage inflation, it would maintain subsidies on food, fuel and fertilizers. Also, to offset a record low in private sector credit, the fiscal policy would support local industries including high-tech and locally made brands.

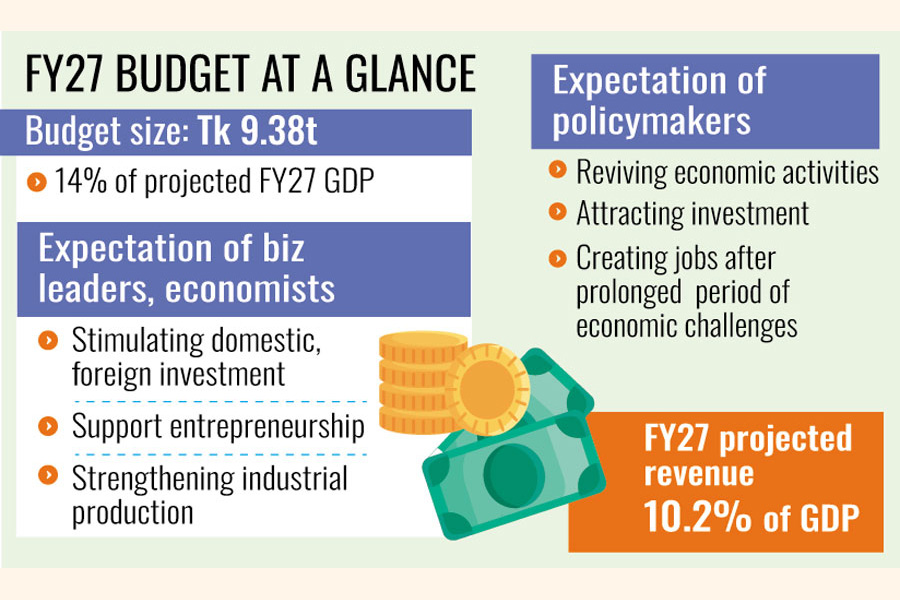

At the same time, to improve the investment climate, the budget would emphasise tax predictability for the business community and offer mechanisms like refunds for excess minimum tax payments. In a similar vein, the government plans to restore soundness of the banking sector, reduce reliance on expensive energy imports by reforming oligarchic market structure to lower LPG and LNG prices. In fact, these are but the wish list that the government plans to implement as part of its fiscal strategy as envisaged in the upcoming budget as proposed. But can the government implement it as planned? Economists consider the Tk9.30 trillion budget for FY27 highly ambitious and therefore not realistic. As such, the budget would face severe implementation hurdles primarily driven by sluggish revenue collection, high inflation, mounting external debt and the banking sector instability. Development spending is particularly at risk, with the Annual Development Programme (ADP) facing chronic underspending due to structural inefficiencies. ADP consistently sees spending rates stuck between 80 per cent and 85 per cent. Implementation of ADP is routinely bottlenecked by delayed procurement processes, poor project design, and complex land acquisition in a densely populated country. The National Board of Revenue (NBR) historically misses its targets, recording a massive structural shortfall. In the previous fiscal year, for instance, the NBR faced unprecedented shortfall. It fell drastically short of its revised target of over Tk4.31 trillion for the July-April, i.e., 10-month period. Despite managing a 10.6 per cent year-on-year growth during this timeframe, it was insufficient to meet the highly ambitious target set for the year. In this connection, some policy think tanks pointed out that the original full-year targets were operationally unrealistic.

That points to deep structural weaknesses, stalled automation and a lack of separation between tax policy and tax implementation. Unsurprisingly, the tax-to-GDP ratio languished between 6.8 per cent to 7.3 per cent. In that case, bankrolling the humongous budget remains questionable seeing that the tax administration has been persistently failing to meet targets year after year. So, reaching the ambitious Tk 6.95 trillion revenue target is severely hindered by systemic tax exemptions and large-scale revenue leakages. Persistent inflation has eroded the general consumers' purchasing power. This inflates government expenditure on subsidies (food, electricity, agriculture) while simultaneously shrinking the overall disposable income of citizens. A significant portion of the budget is devoured by rising domestic debt and interest payments. High government borrowing from the banking sector restricts credit flow to the private sector. Additionally, bad loans and non-performing loans (NPLs) threaten overall banking stability. Private sector credit growth has plummeted to historic lows, stalling industrial growth. The government must shift focus away from theoretically broadening coverage to actually restructuring the NBR. Phasing out inefficient tax exemptions for large conglomerates that generate limited employment will help create a level playing field for all businesses.

To prevent crowding out the private sector, the government should rely more on concessional external financing for high-return projects rather than borrowing from domestic banks. Instead of merely making routine financial statements, development projects should feature strict execution plans and routine monitoring frameworks. Allocating funds to digitised one-stop service platforms will expedite infrastructure delivery. To protect the vulnerable groups amid high inflation, the government can scale up well-targeted programmes, while eliminating overlapping benefits to reduce leakages. These are but some of the prescriptive suggestions as provided by economists and other experts on the subject in different discussion forums from time to time. But can the newly elected BNP government deliver which is only three months in office after February 12's parliamentary election? Given the hurdles as noted in the foregoing, the government is going to come up against enormous challenges. The new administration has no doubt to navigate severe geopolitical and fiscal headwinds including an energy and fiscal emergency that has constrained both public and private sector credit. Most importantly, it will have to focus on addressing the issue of unemployment aggressively. In addition to adopting traditional approach of job creation in the public and private sector, the government should work to expand climate resilient employment. On this score, the BNP government's ambitions programme of excavating and re-excavating 200,000 km of canals and rivers can go a long way towards creating immediate employment opportunity for rural labourers. Educated unemployed youths, on the other hand, can be inspired to create jobs rather than look for employment.

In this regard, the government should give formal recognition to and extend budgetary support for freelancers, content creators and make use of the digital economy to tap into the country's youth demography. Finally, the government has to contain non-performing loans (NPLs) and recapitalise sound banks so that sovereign credit borrowing does not crowd out credit availability for private business. Support for micro-level, small and medium enterprises should lie at the heart of creating jobs for the country's youths.

SYED FATTAHUL ALIM

Published :

Jun 07, 2026 23:01

Updated :

Jun 07, 2026 23:01

A nation's budget for a particular financial year involves the government's comprehensive financial plan outlining its expected revenues and proposed expenditures for the next 12-month accounting period. Actually, the budget reflects the government's economic policies. From the outlines of the proposed budget as provided by the government and discussed by experts, it is going to mark a shift from a debt-driven expansion to one that is focused on macroeconomic stabilisation, broad-based welfare and deregulation. The deregulation understandably involves reducing bureaucratic barriers and slashing the cost of business. Core measures would include separating customs into policy and implementation wings, extending duty-free bonded warehouse privileges to all exporters and establishing a single-point approval system for business licences and registrations.

Since the incumbent government inherited a fragile economy characterized by high inflation and declining private investment, the government's fiscal strategy aims to address these issues through several policy pillars. So, instead of the past practice of heavy central bank borrowing and printing money, the government, as part of investment-led growth, plans to promote domestic production by way of introducing a stimulus package of Tk 600 billion targeting agriculture, CMSMEs and export diversification. To control inflation and ensure social safety, the budget would expand social safety nets prioritising relief for low- and middle-income groups that includes a system of family cards and agricultural loan waivers. On the other hand, to manage inflation, it would maintain subsidies on food, fuel and fertilizers. Also, to offset a record low in private sector credit, the fiscal policy would support local industries including high-tech and locally made brands.

At the same time, to improve the investment climate, the budget would emphasise tax predictability for the business community and offer mechanisms like refunds for excess minimum tax payments. In a similar vein, the government plans to restore soundness of the banking sector, reduce reliance on expensive energy imports by reforming oligarchic market structure to lower LPG and LNG prices. In fact, these are but the wish list that the government plans to implement as part of its fiscal strategy as envisaged in the upcoming budget as proposed. But can the government implement it as planned? Economists consider the Tk9.30 trillion budget for FY27 highly ambitious and therefore not realistic. As such, the budget would face severe implementation hurdles primarily driven by sluggish revenue collection, high inflation, mounting external debt and the banking sector instability. Development spending is particularly at risk, with the Annual Development Programme (ADP) facing chronic underspending due to structural inefficiencies. ADP consistently sees spending rates stuck between 80 per cent and 85 per cent. Implementation of ADP is routinely bottlenecked by delayed procurement processes, poor project design, and complex land acquisition in a densely populated country. The National Board of Revenue (NBR) historically misses its targets, recording a massive structural shortfall. In the previous fiscal year, for instance, the NBR faced unprecedented shortfall. It fell drastically short of its revised target of over Tk4.31 trillion for the July-April, i.e., 10-month period. Despite managing a 10.6 per cent year-on-year growth during this timeframe, it was insufficient to meet the highly ambitious target set for the year. In this connection, some policy think tanks pointed out that the original full-year targets were operationally unrealistic.

That points to deep structural weaknesses, stalled automation and a lack of separation between tax policy and tax implementation. Unsurprisingly, the tax-to-GDP ratio languished between 6.8 per cent to 7.3 per cent. In that case, bankrolling the humongous budget remains questionable seeing that the tax administration has been persistently failing to meet targets year after year. So, reaching the ambitious Tk 6.95 trillion revenue target is severely hindered by systemic tax exemptions and large-scale revenue leakages. Persistent inflation has eroded the general consumers' purchasing power. This inflates government expenditure on subsidies (food, electricity, agriculture) while simultaneously shrinking the overall disposable income of citizens. A significant portion of the budget is devoured by rising domestic debt and interest payments. High government borrowing from the banking sector restricts credit flow to the private sector. Additionally, bad loans and non-performing loans (NPLs) threaten overall banking stability. Private sector credit growth has plummeted to historic lows, stalling industrial growth. The government must shift focus away from theoretically broadening coverage to actually restructuring the NBR. Phasing out inefficient tax exemptions for large conglomerates that generate limited employment will help create a level playing field for all businesses.

To prevent crowding out the private sector, the government should rely more on concessional external financing for high-return projects rather than borrowing from domestic banks. Instead of merely making routine financial statements, development projects should feature strict execution plans and routine monitoring frameworks. Allocating funds to digitised one-stop service platforms will expedite infrastructure delivery. To protect the vulnerable groups amid high inflation, the government can scale up well-targeted programmes, while eliminating overlapping benefits to reduce leakages. These are but some of the prescriptive suggestions as provided by economists and other experts on the subject in different discussion forums from time to time. But can the newly elected BNP government deliver which is only three months in office after February 12's parliamentary election? Given the hurdles as noted in the foregoing, the government is going to come up against enormous challenges. The new administration has no doubt to navigate severe geopolitical and fiscal headwinds including an energy and fiscal emergency that has constrained both public and private sector credit. Most importantly, it will have to focus on addressing the issue of unemployment aggressively. In addition to adopting traditional approach of job creation in the public and private sector, the government should work to expand climate resilient employment. On this score, the BNP government's ambitions programme of excavating and re-excavating 200,000 km of canals and rivers can go a long way towards creating immediate employment opportunity for rural labourers. Educated unemployed youths, on the other hand, can be inspired to create jobs rather than look for employment.

In this regard, the government should give formal recognition to and extend budgetary support for freelancers, content creators and make use of the digital economy to tap into the country's youth demography. Finally, the government has to contain non-performing loans (NPLs) and recapitalise sound banks so that sovereign credit borrowing does not crowd out credit availability for private business. Support for micro-level, small and medium enterprises should lie at the heart of creating jobs for the country's youths.