Bangladesh Defense

Bangladesh DefenseSaif

Senior Member

- Jan 24, 2024

- 20,457

- 9,566

- Nation

- Residence

- Axis Group

Dicey Gulf energy market impacts BB policy

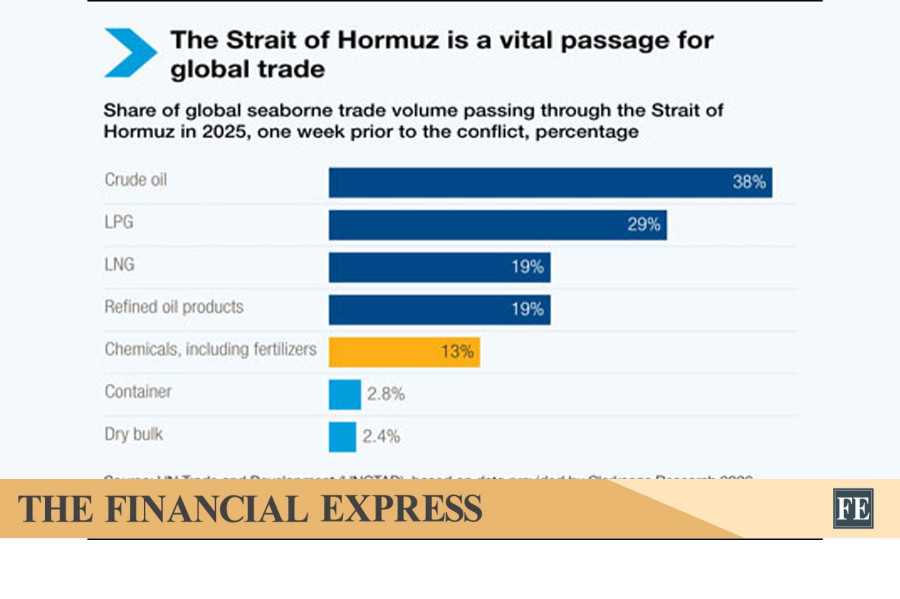

In consequence of the ongoing war in the oil-rich Persian Gulf region following the joint US-Israeli attacks on Iran and the latter's retaliatory measures, the global energy market has, to all appearances, turned upside down overnight. What has raised the worst concern is the virtual shutdown

Dicey Gulf energy market impacts BB policy

SYED FATTAHUL ALIM

Published :

Mar 08, 2026 23:17

Updated :

Mar 08, 2026 23:17

In consequence of the ongoing war in the oil-rich Persian Gulf region following the joint US-Israeli attacks on Iran and the latter's retaliatory measures, the global energy market has, to all appearances, turned upside down overnight. What has raised the worst concern is the virtual shutdown by Iran of the Strait of Hormuz, the chokepoint between Iran and Oman that connects the Persian Gulf to the Arabian Sea. Notably, every day roughly 20 million barrels of oil, which is about 20 to 25 per cent of global oil consumption, and 20 per cent of the liquefied natural gas (LNG), pass through this narrow passage. With Bangladesh's economy so dependent on energy, especially crude oil and Liquefied Natural Gas (LNG) to be particular, from the Gulf countries, the concern of the government here is understandable. The sudden disruption in the supply chain of the Middle Eastern energy has already caused panic among consumers as well as traders. Despite repeated assurances from the government that the country has adequate stock of oil, the local energy market still remains highly volatile.

Needless to say, high energy price means high transportation cost of commodities meaning a fresh upward push to inflation which is already high. Further rise in the inflation, which, according to the Bangladesh Bureau of Statistics (BBS) data, as of January 2026, was hovering around 8.58 or about 9.0 per cent (point-to-point), would put another layer of issues on the existing predicaments of the newly elected BNP government inheriting from the past. Now with sudden crisis in the global energy market, the inflation rate may again reach double-digit figure raising the cost of living further. High inflation also means more depreciation of Bangladesh Taka (BDT) against US dollar (USD) leading to rise in import costs. Instability in the Gulf economies is also linked to the employment situation of our migrant workers in the Middle East and, as such, the remittance dollars they send home. The situation obtaining in the Gulf states amid this war is indeed very precarious where over 8.0 million Bangladesh-origin migrant workers are employed and who sent a record amount of US$32.8 billion last year (2025). Needless to say, these remittance contribute to the nation's economy, particularly to the foreign exchange reserves in a big way. Now that all these countries of the Gulf region are in the heart of the raging destructive war, there is obvious reason for the government to be deeply concerned. Consider that Saudi Arabia hosts over 3.5 million of our expatriate workers, while the United Arab Emirates (UAE) around 2.5 million. The remainders are employed in Oman, Qatar and Bahrain. So, following the start of the current Middle Eastern war which has directly affected all the Gulf states that host Bangladeshi migrant workers, on February 28, their situation has become uncertain. Their job-loss would be a double whammy for the economy as fewer remittance dollars in tandem with increasing number of homebound returnees would render the already fragile economy more insecure. Add to that the issue of imported energy that has been discussed in the foregoing. Against this backdrop, in a bid to find out a way to ride out the emergent crisis, the present governor of the central bank, the Bangladesh Bank (BB), Md Mostaqur Rahman, reportedly took an initiative to meet the country's economists last Saturday (March 7). That is no doubt a prudent move on the part of the new BB governor, who is a businessman with no prior experience of holding a position in any financial organization either in the government, or in the private sector. So, some policy changes such as lowering the policy rate and thus reducing lending costs ostensibly aimed to stimulate economic growth that the new BB governor had been mulling over immediately upon assuming office may be forthcoming. In fact, his predecessor, Ahsan H. Mansur, who was unceremoniously ousted from office, was following a tight monetary policy to check inflation which was not to the liking of a large segment of the business community, who wanted cheaper credit to run their businesses.

Obviously, the fresh Gulf war has upset the calculations of the new BB chief. The top economists of the country he sought opinions from have reportedly advised against lowering the policy rate for now. The issues that featured prominently in the view exchange with the economists evidently centred around the crisis arising from the current war in the Gulf region. Those included first and foremost, the stress it might cause to the reserves of hard currency and saving it for a rainy day. Especially, they advised against spending the reserve dollars for the purpose of import. Also came in their considerations the issue of possible disruption in the inflow of remittance. On the question of disruption of oil and LNG sourced from the Gulf region, the economist were for looking for alternative sources in the Southeast Asia such as Brunei, Malaysia and Singapore. The economist were also against the tendency of instantly passing the cost of any rise in the price of energy in the international market on to the consumers. In fact, a section of the traders, who are unscrupulous, make matters worse by creating an artificial supply crisis. The prevailing panic buying trend following rationing of oil sale from petrol pumps has a lot to blame on the past governments' practice of punishing the consumers in the event of any unforeseen emergency in the energy market. What the consumers have so far experienced is only hike in fuel price come rain or shine. Unfortunately, the consumers were at the receiving end even at times of considerable fall in energy price, for instance, between 2014-15 and 2020-21. But this time around, the culture of making profit by the Bangladesh Petroleum Corporation (BPC), which is a statutory body to import, market and distribute fuels, at the expense of the consumer public, must change. In the evolving circumstances, the new BB governor would do well to listen to the economists and experts and carefully calibrate his options as he might have to resort to measures even to the chagrin of some powerful quarters in politics and businesses.

At this point, one would like him to rise up to his promise he made that he would work with honesty and not bow to any political pressure. Hopefully, he would stand his ground under pressure and put the macroeconomy back on an even keel. That is more so in the face of the past as well as the emerging instabilities in the energy market, which has an overarching impact on the macroeconomy in general and inflation in particular.

SYED FATTAHUL ALIM

Published :

Mar 08, 2026 23:17

Updated :

Mar 08, 2026 23:17

In consequence of the ongoing war in the oil-rich Persian Gulf region following the joint US-Israeli attacks on Iran and the latter's retaliatory measures, the global energy market has, to all appearances, turned upside down overnight. What has raised the worst concern is the virtual shutdown by Iran of the Strait of Hormuz, the chokepoint between Iran and Oman that connects the Persian Gulf to the Arabian Sea. Notably, every day roughly 20 million barrels of oil, which is about 20 to 25 per cent of global oil consumption, and 20 per cent of the liquefied natural gas (LNG), pass through this narrow passage. With Bangladesh's economy so dependent on energy, especially crude oil and Liquefied Natural Gas (LNG) to be particular, from the Gulf countries, the concern of the government here is understandable. The sudden disruption in the supply chain of the Middle Eastern energy has already caused panic among consumers as well as traders. Despite repeated assurances from the government that the country has adequate stock of oil, the local energy market still remains highly volatile.

Needless to say, high energy price means high transportation cost of commodities meaning a fresh upward push to inflation which is already high. Further rise in the inflation, which, according to the Bangladesh Bureau of Statistics (BBS) data, as of January 2026, was hovering around 8.58 or about 9.0 per cent (point-to-point), would put another layer of issues on the existing predicaments of the newly elected BNP government inheriting from the past. Now with sudden crisis in the global energy market, the inflation rate may again reach double-digit figure raising the cost of living further. High inflation also means more depreciation of Bangladesh Taka (BDT) against US dollar (USD) leading to rise in import costs. Instability in the Gulf economies is also linked to the employment situation of our migrant workers in the Middle East and, as such, the remittance dollars they send home. The situation obtaining in the Gulf states amid this war is indeed very precarious where over 8.0 million Bangladesh-origin migrant workers are employed and who sent a record amount of US$32.8 billion last year (2025). Needless to say, these remittance contribute to the nation's economy, particularly to the foreign exchange reserves in a big way. Now that all these countries of the Gulf region are in the heart of the raging destructive war, there is obvious reason for the government to be deeply concerned. Consider that Saudi Arabia hosts over 3.5 million of our expatriate workers, while the United Arab Emirates (UAE) around 2.5 million. The remainders are employed in Oman, Qatar and Bahrain. So, following the start of the current Middle Eastern war which has directly affected all the Gulf states that host Bangladeshi migrant workers, on February 28, their situation has become uncertain. Their job-loss would be a double whammy for the economy as fewer remittance dollars in tandem with increasing number of homebound returnees would render the already fragile economy more insecure. Add to that the issue of imported energy that has been discussed in the foregoing. Against this backdrop, in a bid to find out a way to ride out the emergent crisis, the present governor of the central bank, the Bangladesh Bank (BB), Md Mostaqur Rahman, reportedly took an initiative to meet the country's economists last Saturday (March 7). That is no doubt a prudent move on the part of the new BB governor, who is a businessman with no prior experience of holding a position in any financial organization either in the government, or in the private sector. So, some policy changes such as lowering the policy rate and thus reducing lending costs ostensibly aimed to stimulate economic growth that the new BB governor had been mulling over immediately upon assuming office may be forthcoming. In fact, his predecessor, Ahsan H. Mansur, who was unceremoniously ousted from office, was following a tight monetary policy to check inflation which was not to the liking of a large segment of the business community, who wanted cheaper credit to run their businesses.

Obviously, the fresh Gulf war has upset the calculations of the new BB chief. The top economists of the country he sought opinions from have reportedly advised against lowering the policy rate for now. The issues that featured prominently in the view exchange with the economists evidently centred around the crisis arising from the current war in the Gulf region. Those included first and foremost, the stress it might cause to the reserves of hard currency and saving it for a rainy day. Especially, they advised against spending the reserve dollars for the purpose of import. Also came in their considerations the issue of possible disruption in the inflow of remittance. On the question of disruption of oil and LNG sourced from the Gulf region, the economist were for looking for alternative sources in the Southeast Asia such as Brunei, Malaysia and Singapore. The economist were also against the tendency of instantly passing the cost of any rise in the price of energy in the international market on to the consumers. In fact, a section of the traders, who are unscrupulous, make matters worse by creating an artificial supply crisis. The prevailing panic buying trend following rationing of oil sale from petrol pumps has a lot to blame on the past governments' practice of punishing the consumers in the event of any unforeseen emergency in the energy market. What the consumers have so far experienced is only hike in fuel price come rain or shine. Unfortunately, the consumers were at the receiving end even at times of considerable fall in energy price, for instance, between 2014-15 and 2020-21. But this time around, the culture of making profit by the Bangladesh Petroleum Corporation (BPC), which is a statutory body to import, market and distribute fuels, at the expense of the consumer public, must change. In the evolving circumstances, the new BB governor would do well to listen to the economists and experts and carefully calibrate his options as he might have to resort to measures even to the chagrin of some powerful quarters in politics and businesses.

At this point, one would like him to rise up to his promise he made that he would work with honesty and not bow to any political pressure. Hopefully, he would stand his ground under pressure and put the macroeconomy back on an even keel. That is more so in the face of the past as well as the emerging instabilities in the energy market, which has an overarching impact on the macroeconomy in general and inflation in particular.