Bangladesh Defense

Bangladesh DefenseSaif

Senior Member

- Joined

- Jan 24, 2024

- Messages

- 20,706

- Likes

- 9,684

- Nation

- Residence

- Axis Group

How Bangladesh is reviving its macroeconomy

Although the reforms have just started, some positive results are already visible.

How Bangladesh is reviving its macroeconomy

economic reforms in Bangladesh 2024

VISUAL: SALMAN SAKIB SHAHRYAR

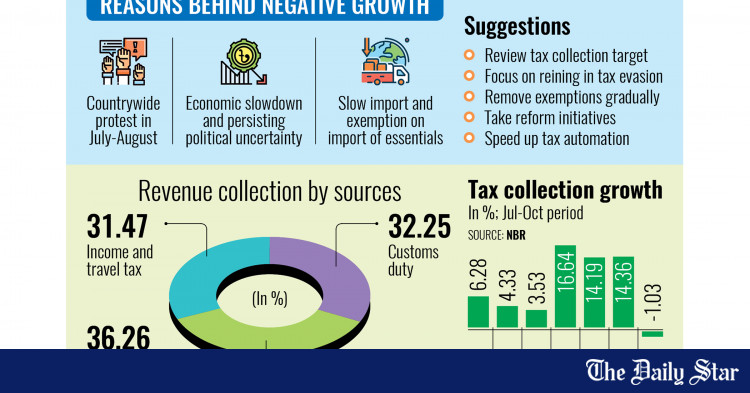

Bangladesh's economy has been on a downward trend since early 2022, marked by high inflation, dwindling foreign exchange reserves, depreciation of the taka, poor health of the banking sector, low and stagnant tax-to-GDP ratio, and falling public spending. GDP growth rate as well as growth in exports and investment rates have been falling too. This downslide is the outcome of poor economic management and endemic corruption, especially thefts in the banking sector and corrupt practices in public procurement.

The dwindling macroeconomy, combined with autocratic and corrupt political governance, rising income inequality and human rights violation, led to the inevitable demise of the previous government on August 5, 2024. An interim government was established, charged with the responsibility of stabilising the macroeconomy and reforming the country's political governance. The most immediate action of this government was to stop the theft-related bleeding of the banking sector by making wholesale changes in the affected banks' management. Second, it fully deregulated the interest rate policy and tightened domestic liquidity by increasing the Bangladesh Bank policy rate. Third, a broad-based fight against corruption, including efforts to recover stolen assets, was announced. Several other reforms now underway include revisiting public spending priorities to cut waste and leakages, reducing corruption and increasing tax collections through online tax filing, lowering duties on essential food imports to reduce inflationary pressure, and mobilising greater financial assistance from multilateral financial institutions.

Although the reforms have just started, some positive results are already visible. The outflow of theft-related bank resources has stopped, demand for credit has slowed, remittances have increased, and deposits are growing. October saw an encouraging recovery in exports. However, inflation remains stubbornly high, the government revenue inflows remain sluggish, and the forex reserves have declined to $18.4 billion as of November 14, down from $20.4 billion in July. This is partly explained by the increase in debt payments and a pickup in imports. Additionally, the expected capital flows from multilateral institutions has not yet materialised, pending the IMF review of the ongoing programme and the time lag in negotiating new BOP financing from the multilateral institutions.

The immediate challenge is to reduce inflation sustainably. And that requires a recovery of imports and manufacturing sector production. More generally, except for domestic resource mobilisation, the demand stabilisation measures are broadly on track. Policy attention now must shift to enhancing imports and augmenting domestic supply, which is intimately linked to the recovery of production, investment and exports.

The supply-side agenda is tough and involves both short-term (one to three years) and medium-term (three-plus years) reforms related to skills, technology, domestic investment, foreign direct investment (FDI), and export diversification. These encompass policy reforms in many areas. The most immediate reforms include:

Exchange rate management: Years of controlled exchange rate management have clearly demonstrated the futility of such a system. The sharp appreciation of the real effective exchange rate between 2011 and 2022 is a major contributor to the present balance of payment crisis. The exchange rate has been slowly liberalised since May 2024 through the unification of multiple exchange rates and adoption of a crawling peg. However, the utility of staying with a crawling peg system is dubious, and it is best to move to a fully flexible market-based exchange rate. The demand management policies in place will protect the rate from fluctuating wildly. A market-based exchange rate is the best way to provide incentives to exporters and remittance senders.

The Bangladesh Bank should also carefully review the outdated foreign currency regime that is riddled with exchange controls and other restrictive practices that impose high transaction costs for exporters and importers, while providing incentives for hundi transactions. Service exports can be boosted through a deregulated and exporter-friendly foreign currency regime.

Monetary policy: As noted, the monetary policy is basically on track. However, more work may be needed to carefully examine the working of the T-bill market. While, in principle, the T-bill market is open to the public, this has become an easy option for banks to make profit for themselves instead of doing lending operations.

Fiscal policy: This presents a huge challenge. Corruption combined with an ineffective tax system has severely constrained tax revenues in Bangladesh. Excessive reliance on indirect taxes has fed into inflation while contributing to income inequality. Similarly, due to weak revenue performance, the total government spending as a share of GDP is low by international standard. Yet, the effectiveness of this limited spending has been reduced by poor spending priorities and corruption. Public spending on health, education, water resources and social protection have been grossly inadequate, while most spending has concentrated on civil service salaries and benefits, subsidies, interest cost and large infrastructure projects. The quality of infrastructure spending has been poor owing to corruption in procurement, contributing to delays and cost overruns.

Clearly, overhauling both tax and expenditure systems is of the highest priority. This is not an easy task and will take several years of sustained effort. The interim government has started to reform both aspects. On the revenue side, it has rightly focused on overhauling the income tax system, where corruption is most endemic. The move to an online system is a smart policy step. But this alone will not yield the full benefits.

To provide incentives to tax filers, two related reforms are essential. First, the tax form must be simplified by doing away with the reconciliation of income, expenditure and wealth. This is a rent-seeking instrument for harassing tax filers and its revenue implications are dubious. Taxpayers enter negotiated settlements with the NBR staff, and the Treasury loses out. Eliminating this requirement would greatly simplify online tax filing and encourage many more filers to go online.

Second, tax audits must be automated based on pre-selected triggers and be highly selective, mostly focused on large taxpayers. Full documentation including income and wealth reconciliation become relevant during an audit review.

Regarding expenditure management, a top priority is to cut back on fossil fuel subsidies and large infrastructure projects and increase spending on health, education, water resources and social protection. In the present environment of high inflation, higher spending on social protection with a focus on the poor is essential.

Meaningful property tax: Local government institutions—i.e. city corporations and municipalities—are ineffective because of heavy resource constraints. Global experience shows that the best instrument for augmenting their finances is through the institution of a meaningful property tax system that is based on market value of properties and a meaningful tax rate. Substantial revenues can be collected from this reform that will ease the pressure on treasury transfers to these institutions.

State-owned enterprises (SoEs): SoEs are draining the scarce fiscal resources of the Treasury with poor financial performance. The total book value of SoE assets in FY2021 was estimated at 16 percent of GDP, yet the net fiscal transfers to these SoEs was in the range of two to three percent of GDP. I prepared a detailed report on how the financial performance of SoEs can be improved and shared this with the finance ministry in early 2024. The core reforms involve corporate governance and pricing policy. This is a low-hanging fruit, which the interim government may want to focus on.

Trade policy: A sharp reduction in trade taxes is essential to diversify and boost exports. Doing so will also reduce inflation. Government revenues must be raised through income taxation and VAT. The trade policy should focus on supporting the expansion of manufacturing exports and limited support for well-established import substitutes.

Investment climate: Reversing the downturn in private investment and attracting FDI will require sharp improvement in the investment climate. Establishing law and order, including protection of private property, is the topmost priority. Resolution of labour disputes is another priority. Restoring the confidence of the domestic private sector is essential to attract FDI. Easing of foreign currency regulations and imports, provision of uninterrupted power supply, and tax and trade policy reforms will all help improve the investment climate.

Dr Sadiq Ahmed is vice-chairman at the Policy Research Institute of Bangladesh (PRI).

economic reforms in Bangladesh 2024

VISUAL: SALMAN SAKIB SHAHRYAR

Bangladesh's economy has been on a downward trend since early 2022, marked by high inflation, dwindling foreign exchange reserves, depreciation of the taka, poor health of the banking sector, low and stagnant tax-to-GDP ratio, and falling public spending. GDP growth rate as well as growth in exports and investment rates have been falling too. This downslide is the outcome of poor economic management and endemic corruption, especially thefts in the banking sector and corrupt practices in public procurement.

The dwindling macroeconomy, combined with autocratic and corrupt political governance, rising income inequality and human rights violation, led to the inevitable demise of the previous government on August 5, 2024. An interim government was established, charged with the responsibility of stabilising the macroeconomy and reforming the country's political governance. The most immediate action of this government was to stop the theft-related bleeding of the banking sector by making wholesale changes in the affected banks' management. Second, it fully deregulated the interest rate policy and tightened domestic liquidity by increasing the Bangladesh Bank policy rate. Third, a broad-based fight against corruption, including efforts to recover stolen assets, was announced. Several other reforms now underway include revisiting public spending priorities to cut waste and leakages, reducing corruption and increasing tax collections through online tax filing, lowering duties on essential food imports to reduce inflationary pressure, and mobilising greater financial assistance from multilateral financial institutions.

Although the reforms have just started, some positive results are already visible. The outflow of theft-related bank resources has stopped, demand for credit has slowed, remittances have increased, and deposits are growing. October saw an encouraging recovery in exports. However, inflation remains stubbornly high, the government revenue inflows remain sluggish, and the forex reserves have declined to $18.4 billion as of November 14, down from $20.4 billion in July. This is partly explained by the increase in debt payments and a pickup in imports. Additionally, the expected capital flows from multilateral institutions has not yet materialised, pending the IMF review of the ongoing programme and the time lag in negotiating new BOP financing from the multilateral institutions.

The immediate challenge is to reduce inflation sustainably. And that requires a recovery of imports and manufacturing sector production. More generally, except for domestic resource mobilisation, the demand stabilisation measures are broadly on track. Policy attention now must shift to enhancing imports and augmenting domestic supply, which is intimately linked to the recovery of production, investment and exports.

The supply-side agenda is tough and involves both short-term (one to three years) and medium-term (three-plus years) reforms related to skills, technology, domestic investment, foreign direct investment (FDI), and export diversification. These encompass policy reforms in many areas. The most immediate reforms include:

Exchange rate management: Years of controlled exchange rate management have clearly demonstrated the futility of such a system. The sharp appreciation of the real effective exchange rate between 2011 and 2022 is a major contributor to the present balance of payment crisis. The exchange rate has been slowly liberalised since May 2024 through the unification of multiple exchange rates and adoption of a crawling peg. However, the utility of staying with a crawling peg system is dubious, and it is best to move to a fully flexible market-based exchange rate. The demand management policies in place will protect the rate from fluctuating wildly. A market-based exchange rate is the best way to provide incentives to exporters and remittance senders.

The Bangladesh Bank should also carefully review the outdated foreign currency regime that is riddled with exchange controls and other restrictive practices that impose high transaction costs for exporters and importers, while providing incentives for hundi transactions. Service exports can be boosted through a deregulated and exporter-friendly foreign currency regime.

Monetary policy: As noted, the monetary policy is basically on track. However, more work may be needed to carefully examine the working of the T-bill market. While, in principle, the T-bill market is open to the public, this has become an easy option for banks to make profit for themselves instead of doing lending operations.

Fiscal policy: This presents a huge challenge. Corruption combined with an ineffective tax system has severely constrained tax revenues in Bangladesh. Excessive reliance on indirect taxes has fed into inflation while contributing to income inequality. Similarly, due to weak revenue performance, the total government spending as a share of GDP is low by international standard. Yet, the effectiveness of this limited spending has been reduced by poor spending priorities and corruption. Public spending on health, education, water resources and social protection have been grossly inadequate, while most spending has concentrated on civil service salaries and benefits, subsidies, interest cost and large infrastructure projects. The quality of infrastructure spending has been poor owing to corruption in procurement, contributing to delays and cost overruns.

Clearly, overhauling both tax and expenditure systems is of the highest priority. This is not an easy task and will take several years of sustained effort. The interim government has started to reform both aspects. On the revenue side, it has rightly focused on overhauling the income tax system, where corruption is most endemic. The move to an online system is a smart policy step. But this alone will not yield the full benefits.

To provide incentives to tax filers, two related reforms are essential. First, the tax form must be simplified by doing away with the reconciliation of income, expenditure and wealth. This is a rent-seeking instrument for harassing tax filers and its revenue implications are dubious. Taxpayers enter negotiated settlements with the NBR staff, and the Treasury loses out. Eliminating this requirement would greatly simplify online tax filing and encourage many more filers to go online.

Second, tax audits must be automated based on pre-selected triggers and be highly selective, mostly focused on large taxpayers. Full documentation including income and wealth reconciliation become relevant during an audit review.

Regarding expenditure management, a top priority is to cut back on fossil fuel subsidies and large infrastructure projects and increase spending on health, education, water resources and social protection. In the present environment of high inflation, higher spending on social protection with a focus on the poor is essential.

Meaningful property tax: Local government institutions—i.e. city corporations and municipalities—are ineffective because of heavy resource constraints. Global experience shows that the best instrument for augmenting their finances is through the institution of a meaningful property tax system that is based on market value of properties and a meaningful tax rate. Substantial revenues can be collected from this reform that will ease the pressure on treasury transfers to these institutions.

State-owned enterprises (SoEs): SoEs are draining the scarce fiscal resources of the Treasury with poor financial performance. The total book value of SoE assets in FY2021 was estimated at 16 percent of GDP, yet the net fiscal transfers to these SoEs was in the range of two to three percent of GDP. I prepared a detailed report on how the financial performance of SoEs can be improved and shared this with the finance ministry in early 2024. The core reforms involve corporate governance and pricing policy. This is a low-hanging fruit, which the interim government may want to focus on.

Trade policy: A sharp reduction in trade taxes is essential to diversify and boost exports. Doing so will also reduce inflation. Government revenues must be raised through income taxation and VAT. The trade policy should focus on supporting the expansion of manufacturing exports and limited support for well-established import substitutes.

Investment climate: Reversing the downturn in private investment and attracting FDI will require sharp improvement in the investment climate. Establishing law and order, including protection of private property, is the topmost priority. Resolution of labour disputes is another priority. Restoring the confidence of the domestic private sector is essential to attract FDI. Easing of foreign currency regulations and imports, provision of uninterrupted power supply, and tax and trade policy reforms will all help improve the investment climate.

Dr Sadiq Ahmed is vice-chairman at the Policy Research Institute of Bangladesh (PRI).