Bangladesh Defense

Bangladesh DefenseSaif

Senior Member

- Jan 24, 2024

- 20,382

- 9,555

- Nation

- Residence

- Axis Group

Gross forex reserves dip below $20b again

The gross foreign exchange reserves in Bangladesh, according to the International Monetary Fund guidelines, dropped to $19.98 billion...

www.newagebd.net

www.newagebd.net

Gross forex reserves dip below $20b again

Staff Correspondent | Published: 23:09, Mar 21,2024

A file photo shows a man counting dollar notes in the capital Dhaka. The gross foreign exchange reserves in Bangladesh, according to the International Monetary Fund guidelines, dropped to $19.98 billion on Wednesday. — New Age photo

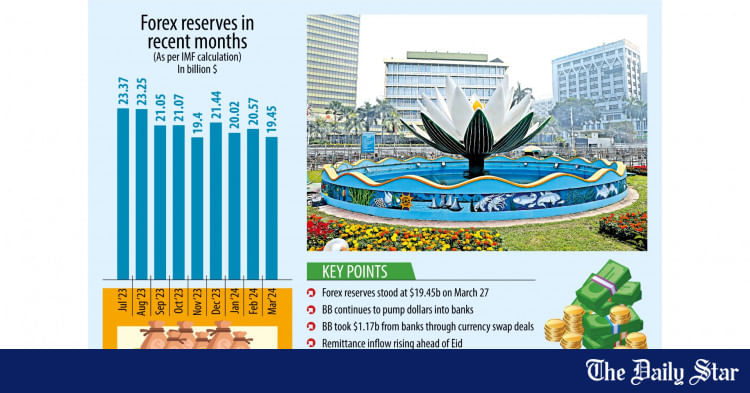

The gross foreign exchange reserves in Bangladesh, according to the International Monetary Fund guidelines, dropped to $19.98 billion on Wednesday.

According to Bangladesh Bank data, the foreign exchange reserves reached the current level on the day from $20.78 billion at the end of January 2024 and $21.86 billion at the end of December 2023.

However, based on the Bangladesh Bank’s conventional valuation, the foreign exchange reserves were reported as $25.24 billion on that day.

The reserves did not fall significantly as the central bank received more than $1 billion from banks under recently launched swap arrangements, bankers said.

As the banks are facing serious liquidity crisis, they are searching for options for local currency under the arrangements, they said.

So, the dollar rate declined by Tk 4-6 each on the open market to Tk 117 each.

The foreign exchange reserves had previously dropped to $19.13 billion on December 6, 2023, but recovered to $21.74 billion on January 4 after receiving $689 million in loans from the International Monetary Fund and $400 million from the Asian Development Bank.

The Bangladesh Bank follows the IMF’s BPM6 for calculating gross and net international reserves.

The decline in the country’s foreign exchange reserves continued due mainly to a significant dollar shortage on the market, which has compelled the central bank to continue selling dollars to the banks from its reserves, BB officials said.

Due to payments made to the Asian Clearing Union, the reserves also declined.

The Asian Clearing Union is a payment settlement forum whereby the participants settle payments for intra-regional transactions through participating central banks on a net multilateral basis.

Payment obligations of transactions among Bangladesh, Bhutan, India, Iran, the Maldives, Myanmar, Nepal, Pakistan and Sri Lanka are settled through the ACU payment system.

Apart from the payment obligations to ACU, the ongoing sales of foreign currency to the country’s banks by the central bank contributed to the reduction in the country’s foreign exchange reserves.

The central bank has been selling dollars to commercial banks, with more than $30 billion sold over the past 32 months.

This included $9 billion allocated to banks in July-February of the financial year 2023-24, $13.5 billion in FY23 and $7.62 billion in FY22.

Staff Correspondent | Published: 23:09, Mar 21,2024

A file photo shows a man counting dollar notes in the capital Dhaka. The gross foreign exchange reserves in Bangladesh, according to the International Monetary Fund guidelines, dropped to $19.98 billion on Wednesday. — New Age photo

The gross foreign exchange reserves in Bangladesh, according to the International Monetary Fund guidelines, dropped to $19.98 billion on Wednesday.

According to Bangladesh Bank data, the foreign exchange reserves reached the current level on the day from $20.78 billion at the end of January 2024 and $21.86 billion at the end of December 2023.

However, based on the Bangladesh Bank’s conventional valuation, the foreign exchange reserves were reported as $25.24 billion on that day.

The reserves did not fall significantly as the central bank received more than $1 billion from banks under recently launched swap arrangements, bankers said.

As the banks are facing serious liquidity crisis, they are searching for options for local currency under the arrangements, they said.

So, the dollar rate declined by Tk 4-6 each on the open market to Tk 117 each.

The foreign exchange reserves had previously dropped to $19.13 billion on December 6, 2023, but recovered to $21.74 billion on January 4 after receiving $689 million in loans from the International Monetary Fund and $400 million from the Asian Development Bank.

The Bangladesh Bank follows the IMF’s BPM6 for calculating gross and net international reserves.

The decline in the country’s foreign exchange reserves continued due mainly to a significant dollar shortage on the market, which has compelled the central bank to continue selling dollars to the banks from its reserves, BB officials said.

Due to payments made to the Asian Clearing Union, the reserves also declined.

The Asian Clearing Union is a payment settlement forum whereby the participants settle payments for intra-regional transactions through participating central banks on a net multilateral basis.

Payment obligations of transactions among Bangladesh, Bhutan, India, Iran, the Maldives, Myanmar, Nepal, Pakistan and Sri Lanka are settled through the ACU payment system.

Apart from the payment obligations to ACU, the ongoing sales of foreign currency to the country’s banks by the central bank contributed to the reduction in the country’s foreign exchange reserves.

The central bank has been selling dollars to commercial banks, with more than $30 billion sold over the past 32 months.

This included $9 billion allocated to banks in July-February of the financial year 2023-24, $13.5 billion in FY23 and $7.62 billion in FY22.