Bangladesh Defense

Bangladesh Defense- Jan 24, 2024

- 4,015

- 2,194

Banks shun old-time Motijheel for glitzy Gulshan

Motijheel is losing its historic lustre as Dhaka’s commercial hub, with Gulshan, among the wealthiest neighbourhoods in the capital, stealing its thunder.www.thedailystar.net

Banks shun old-time Motijheel for glitzy Gulshan

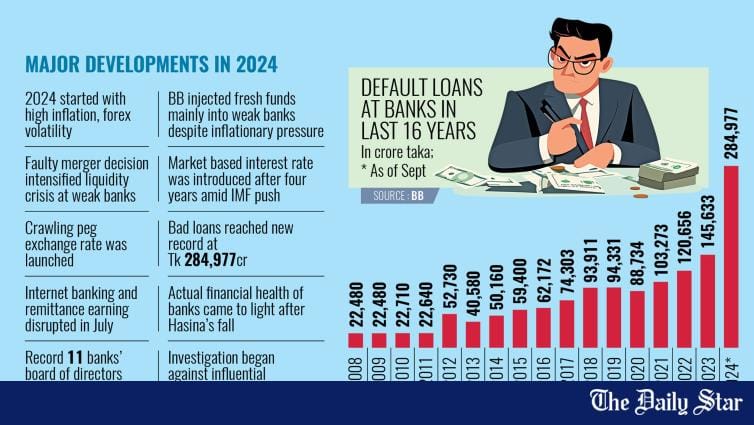

View attachment 11437

Motijheel is losing its historic lustre as Dhaka's commercial hub, with Gulshan, among the wealthiest neighbourhoods in the capital, stealing its thunder.

Nearly half of the country's 61 banks and 35 non-bank financial institutions (NBFIs) have shifted their head offices from Motijheel to Gulshan in the past decade while many others harbour aspirations of moving to what has quickly become the most appealing zip code.

Not only that, but even newly licensed banks, NBFIs and insurance companies have established head offices in Gulshan despite the fact that the Bangladesh Bank is still situated in Motijheel.

For example, Bengal Commercial Bank, awarded a Bangladesh Bank licence in 2020, established its head office in Gulshan. The same is true for Community Bank Bangladesh, licensed in 2018.

Industry people said major factors for this trend include changing business and economy, proximity to the offices of some of the largest corporations in the country as well as hotels and shopping malls, and a lack of modernisation of the Motijheel area.

"Most factories are situated in Gazipur, Ashulia, Tongi and Uttara. So it is punishing for our clients to visit Motijheel. Most of them feel Gulshan is more convenient. That is why banks are so keen to shift their head offices to the area," Mosleh Uddin Ahmed, managing director of Shahjalal Islami Bank, told The Daily Star.

Ahmed outlined another key reason for the Shariah-based lender shifting its head office from Motijheel to Gulshan Avenue in 2014, saying: "Most luxury hotels and shopping malls are located in Gulshan, making it convenient for foreign buyers who visit banks with our local customers."

He added that a major portion of clients now reside in Uttara, Gulshan, Banani and Dhanmondi, making it easier to visit Gulshan compared to Motijheel, adding that the latter offered only one benefit.

View attachment 11438

"Bangladesh Bank is located in Motijheel, which is the only convenient factor for banks and financial institutions."

The senior banker added that the Motijheel area has been stagnant in terms of development while Gulshan and Uttara were prospering through the expansion of infrastructure and industries.

M Khurshed Alam, deputy managing director of Eastern Bank, which now also boasts a Gulshan address, told The Daily Star that most banks want to be in the vicinity of big corporate houses and businesses, a majority of which are situated in Gulshan and Uttara.

"Similarly, a majority of manufacturing units are located in Gazipur, Bhaluka and Mymensingh. So, banks are shifting their head offices to Gulshan," he said.

Alam added that foreign buyers also prefer Gulshan and Banani instead of Motijheel since those areas are closer to the Dhaka airport.

You will Insha-Allah see another shift to a newer part of Dhaka further North to newer neighborhoods around Jolshiri's DHA/DOHS commercial hub in another ten or so years.