Bangladesh Defense Forum

Bangladesh Defense Forum- Copy to clipboard

- Thread starter

- #91

Saif

Senior Member

- Jan 24, 2024

- 11,686

- 6,563

- Origin

- Residence

- Axis Group

No bank will be closed

Although some banks are going through a crisis, no bank will be shut down, Finance Adviser Salehuddin Ahmed said as he urged depositors not to panic.

No bank will be closed

Salehuddin says

Although some banks are going through a crisis, no bank will be shut down, Finance Adviser Salehuddin Ahmed said as he urged depositors not to panic.

He made the remarks while addressing a press conference at the Secretariat yesterday, reiterating the stance that Bangladesh Bank Governor Ahsan H Mansur had taken the prior day.

"Some banks are crawling while others such as Islami Bank have recovered already. But I want to assure depositors that no bank will be shut down," Ahmed said during a media briefing to mark 100 days of the interim government.

The banking sector in Bangladesh has been facing a series of crises in recent years, marked by rising non-performing loans (NPLs), liquidity shortages, and governance challenges.

The banking sector has been facing a series of crises in recent years, marked by rising NPLs, liquidity shortages, and governance challenges

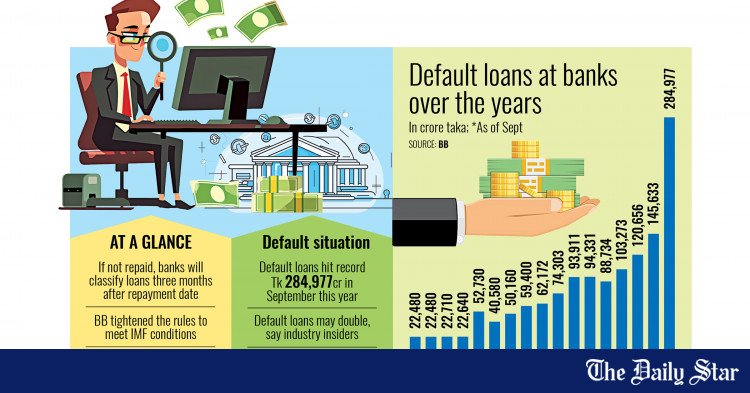

Bad loans hit a record Tk 284,977 crore at the end of September, fuelled by weak enforcement of regulations, political interference, and inadequate credit risk assessment during the regime of the recently ousted Awami League-led government.

Some private Shariah-based banks and a few state-owned banks were at the centre of controversy, becoming embroiled in massive loan irregularities that were often linked to companies and borrowers with affiliations to the previous government.

This eroded public confidence and created operational challenges, including cash shortages.

Highlighting various irregularities under the past government's watch, Ahmed said policies taken at that time were not bad, but they were not implemented properly.

However, after taking charge, the interim government has assumed the responsibility to salvage the banking sector and efforts are being made to this end, the finance adviser said.

For example, ailing banks are getting liquidity support from the inter-bank money market, he said.

"Depositors kept their hard-earned money in banks so efforts will continue in order to ensure that deposits are unaffected," he added.

Ahmed also said various reforms to the banking sector have been initiated, adding that laws are being amended and that reforms would be made to the central bank as well.

He stressed that the job of the central bank is only to supervise, inspect and audit.

"I heard audit reports were previously sent to the central bank governor and deputy governor for approval. And if those reports impacted any influential person, then they would be scrapped. That should not happen. Measures should be taken according to the findings of the audit report."

Ahmed also urged businessmen to move ahead without fear.

He said that some people are saying that businessmen are fearful but added that honest entrepreneurs should not be afraid. Those involved in irregularities have reason to be scared although many have already fled the country, he added.

During the briefing, the finance adviser also addressed the impact on small investors in the stock market, acknowledging their losses from investments in poor performers. Compensation measures are being considered, according to Ahmed.

Finance Secretary Md Khairuzzaman Mozumder, Financial Institutions Division Secretary Nazma Mobarek, Economic Relations Division Secretary Md Shahriar Kader Siddiky and National Board of Revenue Chairman Md Abdur Rahman Khan were present at the press conference.

Salehuddin says

Although some banks are going through a crisis, no bank will be shut down, Finance Adviser Salehuddin Ahmed said as he urged depositors not to panic.

He made the remarks while addressing a press conference at the Secretariat yesterday, reiterating the stance that Bangladesh Bank Governor Ahsan H Mansur had taken the prior day.

"Some banks are crawling while others such as Islami Bank have recovered already. But I want to assure depositors that no bank will be shut down," Ahmed said during a media briefing to mark 100 days of the interim government.

The banking sector in Bangladesh has been facing a series of crises in recent years, marked by rising non-performing loans (NPLs), liquidity shortages, and governance challenges.

The banking sector has been facing a series of crises in recent years, marked by rising NPLs, liquidity shortages, and governance challenges

Bad loans hit a record Tk 284,977 crore at the end of September, fuelled by weak enforcement of regulations, political interference, and inadequate credit risk assessment during the regime of the recently ousted Awami League-led government.

Some private Shariah-based banks and a few state-owned banks were at the centre of controversy, becoming embroiled in massive loan irregularities that were often linked to companies and borrowers with affiliations to the previous government.

This eroded public confidence and created operational challenges, including cash shortages.

Highlighting various irregularities under the past government's watch, Ahmed said policies taken at that time were not bad, but they were not implemented properly.

However, after taking charge, the interim government has assumed the responsibility to salvage the banking sector and efforts are being made to this end, the finance adviser said.

For example, ailing banks are getting liquidity support from the inter-bank money market, he said.

"Depositors kept their hard-earned money in banks so efforts will continue in order to ensure that deposits are unaffected," he added.

Ahmed also said various reforms to the banking sector have been initiated, adding that laws are being amended and that reforms would be made to the central bank as well.

He stressed that the job of the central bank is only to supervise, inspect and audit.

"I heard audit reports were previously sent to the central bank governor and deputy governor for approval. And if those reports impacted any influential person, then they would be scrapped. That should not happen. Measures should be taken according to the findings of the audit report."

Ahmed also urged businessmen to move ahead without fear.

He said that some people are saying that businessmen are fearful but added that honest entrepreneurs should not be afraid. Those involved in irregularities have reason to be scared although many have already fled the country, he added.

During the briefing, the finance adviser also addressed the impact on small investors in the stock market, acknowledging their losses from investments in poor performers. Compensation measures are being considered, according to Ahmed.

Finance Secretary Md Khairuzzaman Mozumder, Financial Institutions Division Secretary Nazma Mobarek, Economic Relations Division Secretary Md Shahriar Kader Siddiky and National Board of Revenue Chairman Md Abdur Rahman Khan were present at the press conference.