Bangladesh Defense

Bangladesh DefenseSaif

Senior Member

- Jan 24, 2024

- 20,562

- 9,607

- Nation

- Residence

- Axis Group

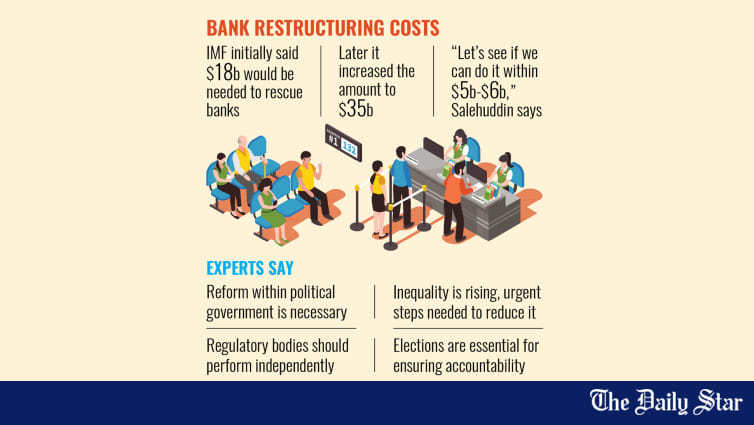

Banking fix may cost $5b-$6b

The interim government is considering a rescue plan costing around $5 to $6 billion to salvage troubled banks, which are reeling from widespread irregularities during the previous Awami League government, said Finance Adviser Salehuddin Ahmed.

Banking fix may cost $5b-$6b

Says finance adviser; the amount is way below IMF’s $35b estimate

The interim government is considering a rescue plan costing around $5 to $6 billion to salvage troubled banks, which are reeling from widespread irregularities during the previous Awami League government, said Finance Adviser Salehuddin Ahmed.

This is way below the International Monetary Fund's (IMF) initial estimate of $18 billion, which was later raised to $35 billion.

"The IMF asked us where we would get such a whopping amount. I told them let's see if we can restructure them within $5 billion to $6 billion," Ahmed said at a book launch in Dhaka yesterday.

Former caretaker government adviser Hossain Zillur Rahman's book "Arthoniti, Shashon, O Khamota: Japito Jiboner Alekkho" was unveiled at the programme. BNP Secretary General Mirza Fakhrul Islam Alamgir was also present.

Ahmed said the interim government had inherited an economy on the brink of collapse, but signs of recovery are now beginning to show.

"But it is not fully recovered yet, and a total cure is not a simple task," he added.

Commenting on the scale of economic mismanagement and plundering during the previous government, Ahmed said, "Such looting was not seen in any country in the world."

The interim government is carrying out short-term reforms, while long-term and mid-term reforms will be undertaken by a political government-— Salehuddin Ahmed Finance adviser.

He claimed that up to 80 percent of loans from some banks had been siphoned off.

"For instance, the total outstanding loan of a bank is Tk 20,000 crore, while around Tk 16,000 crore was taken away and they are now bad loans," said Ahmed, an economist and former governor of the central bank.

He questioned whether any public institution remained unaffected. "The law was broken. Process and system were distorted to such a level, it is difficult to do a good task," he said.

He noted that while the institutions remained in place, those responsible for the decay had not been replaced.

"Some people called to depart them all. However, an administration cannot run in such a way. So, we are trying to make them work by either gently persuading or scolding them. A countervailing power is necessary in the government," said the adviser.

Ensuring good governance under the existing political structure is extremely difficult, as there are no effective checks and balances on the prime minister and members of parliament, he said.

"Without reforms here, no matter how many reforms we talk about, it would not make any difference. Reforms are also needed within political parties," said the finance adviser.

He said that while the interim government is working on short-term reforms, it will be up to an elected political administration to carry out long-term and mid-term changes.

"I have realised that it is easy to exploit, but difficult to govern people here," he said.

BNP Secretary General Mirza Fakhrul Islam Alamgir said reforms are needed, but that must not be used as a pretext to delay elections.

"Reforms cannot be carried out overnight, and they take time. So democratic practices should not be delayed for the sake of reforms," Fakhrul said, adding, "Reforms must be made by people's representatives elected through a democratic process."

At the programme, Professor Mahbub Ullah, former chair of the Department of Development Studies at Dhaka University, focused on addressing rising inequality.

Fahmida Khatun, executive director at local think tank Centre for Policy Dialogue (CPD), said good governance is possible only if accountability is ensured, political stability is maintained, law enforcement remains effective, and regulators operate properly.

Despite high GDP growth and development over the past 15 years, most people had not benefited due to poor governance and corruption, she added.

"During this period, it was forgotten that people are at the centre of power," said the economist. "Regulatory bodies such as the Bangladesh Bank, the Bangladesh Securities and Exchange Commission, and the National Board of Revenue lost their institutional strength. As a result, a vested group benefited."

Prof Abu Ahmed, chairman of the Investment Corporation of Bangladesh (ICB), said he found the institution stripped of all assets when he was appointed. "It is a policy of autocracy that creates 'Mafiaism' and loots institutions. ICB was one victim of such an act."

He recommended elections, even if they might not resolve every issue. "Leaders should be elected, which will make them accountable," he said, adding that there must be a system to ensure no one can become an autocrat again, as autocracy damages the economy.

Hossain Zillur Rahman highlighted three essential conditions for reform and good governance.

First, he said, the democratic framework should prevent any individual or group, including within political parties, from becoming the sole source of power. During the previous regime, not only the prime minister but also all 300 parliamentarians acted as power centres in their own constituencies.

Rahman called for the decentralisation of power.

Second, he said the country should be made capable in terms of institutional functionality. Third, democratic behaviour must be practised and embedded immediately.

"It may take time, but there is no way to sit idle, saying it will take time. So practice should start," he said.

The book was published by Aloghar Prakashana. M Humayun Kabir, president of the Bangladesh Enterprise Institute, also spoke at the launch.

Says finance adviser; the amount is way below IMF’s $35b estimate

The interim government is considering a rescue plan costing around $5 to $6 billion to salvage troubled banks, which are reeling from widespread irregularities during the previous Awami League government, said Finance Adviser Salehuddin Ahmed.

This is way below the International Monetary Fund's (IMF) initial estimate of $18 billion, which was later raised to $35 billion.

"The IMF asked us where we would get such a whopping amount. I told them let's see if we can restructure them within $5 billion to $6 billion," Ahmed said at a book launch in Dhaka yesterday.

Former caretaker government adviser Hossain Zillur Rahman's book "Arthoniti, Shashon, O Khamota: Japito Jiboner Alekkho" was unveiled at the programme. BNP Secretary General Mirza Fakhrul Islam Alamgir was also present.

Ahmed said the interim government had inherited an economy on the brink of collapse, but signs of recovery are now beginning to show.

"But it is not fully recovered yet, and a total cure is not a simple task," he added.

Commenting on the scale of economic mismanagement and plundering during the previous government, Ahmed said, "Such looting was not seen in any country in the world."

The interim government is carrying out short-term reforms, while long-term and mid-term reforms will be undertaken by a political government-— Salehuddin Ahmed Finance adviser.

He claimed that up to 80 percent of loans from some banks had been siphoned off.

"For instance, the total outstanding loan of a bank is Tk 20,000 crore, while around Tk 16,000 crore was taken away and they are now bad loans," said Ahmed, an economist and former governor of the central bank.

He questioned whether any public institution remained unaffected. "The law was broken. Process and system were distorted to such a level, it is difficult to do a good task," he said.

He noted that while the institutions remained in place, those responsible for the decay had not been replaced.

"Some people called to depart them all. However, an administration cannot run in such a way. So, we are trying to make them work by either gently persuading or scolding them. A countervailing power is necessary in the government," said the adviser.

Ensuring good governance under the existing political structure is extremely difficult, as there are no effective checks and balances on the prime minister and members of parliament, he said.

"Without reforms here, no matter how many reforms we talk about, it would not make any difference. Reforms are also needed within political parties," said the finance adviser.

He said that while the interim government is working on short-term reforms, it will be up to an elected political administration to carry out long-term and mid-term changes.

"I have realised that it is easy to exploit, but difficult to govern people here," he said.

BNP Secretary General Mirza Fakhrul Islam Alamgir said reforms are needed, but that must not be used as a pretext to delay elections.

"Reforms cannot be carried out overnight, and they take time. So democratic practices should not be delayed for the sake of reforms," Fakhrul said, adding, "Reforms must be made by people's representatives elected through a democratic process."

At the programme, Professor Mahbub Ullah, former chair of the Department of Development Studies at Dhaka University, focused on addressing rising inequality.

Fahmida Khatun, executive director at local think tank Centre for Policy Dialogue (CPD), said good governance is possible only if accountability is ensured, political stability is maintained, law enforcement remains effective, and regulators operate properly.

Despite high GDP growth and development over the past 15 years, most people had not benefited due to poor governance and corruption, she added.

"During this period, it was forgotten that people are at the centre of power," said the economist. "Regulatory bodies such as the Bangladesh Bank, the Bangladesh Securities and Exchange Commission, and the National Board of Revenue lost their institutional strength. As a result, a vested group benefited."

Prof Abu Ahmed, chairman of the Investment Corporation of Bangladesh (ICB), said he found the institution stripped of all assets when he was appointed. "It is a policy of autocracy that creates 'Mafiaism' and loots institutions. ICB was one victim of such an act."

He recommended elections, even if they might not resolve every issue. "Leaders should be elected, which will make them accountable," he said, adding that there must be a system to ensure no one can become an autocrat again, as autocracy damages the economy.

Hossain Zillur Rahman highlighted three essential conditions for reform and good governance.

First, he said, the democratic framework should prevent any individual or group, including within political parties, from becoming the sole source of power. During the previous regime, not only the prime minister but also all 300 parliamentarians acted as power centres in their own constituencies.

Rahman called for the decentralisation of power.

Second, he said the country should be made capable in terms of institutional functionality. Third, democratic behaviour must be practised and embedded immediately.

"It may take time, but there is no way to sit idle, saying it will take time. So practice should start," he said.

The book was published by Aloghar Prakashana. M Humayun Kabir, president of the Bangladesh Enterprise Institute, also spoke at the launch.