Bangladesh Defense

Bangladesh DefenseSaif

Senior Member

- Jan 24, 2024

- 20,500

- 9,589

- Nation

- Residence

- Axis Group

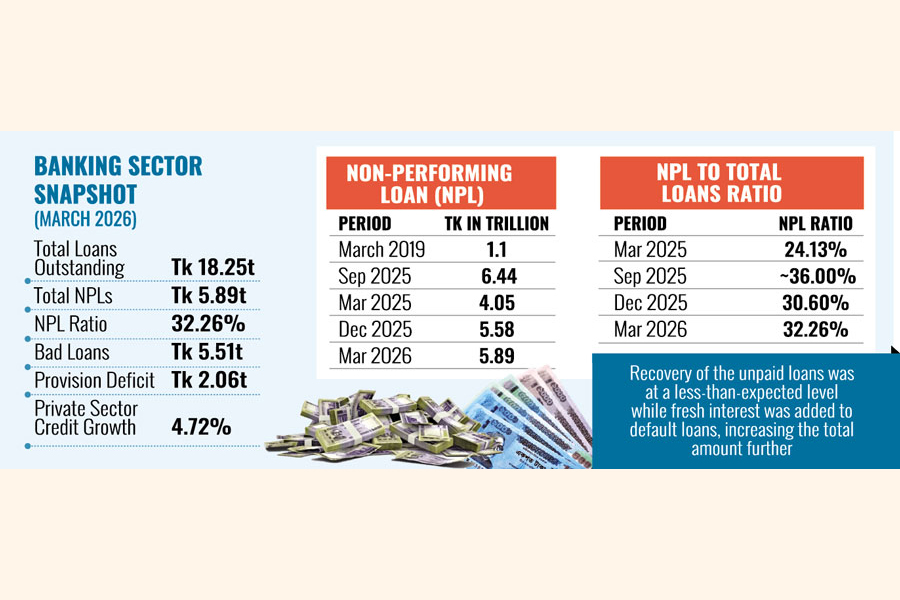

Pvt sector credit growth hits record low of 4.72pc

Private sector credit growth in Bangladesh fell to a historic low of 4.72 per cent in March 2026, reflecting sluggish business activities, weak investment appetite and continued stress across the economy...

www.newagebd.net

www.newagebd.net

Pvt sector credit growth hits record low of 4.72pc

Staff Correspondent 20 May, 2026, 23:28

A file photo shows a man counting taka notes in the capital. | New Age photo

Private sector credit growth in Bangladesh fell to a historic low of 4.72 per cent in March 2026, reflecting sluggish business activities, weak investment appetite and continued stress across the economy.

According to data from Bangladesh Bank, private sector credit growth declined sharply 6.03 per cent in both January and February and 6.1 per cent in December, extending the prolonged slowdown in bank lending to businesses.

The March figure marked the lowest level in Bangladesh Bank’s recorded history since it began compiling private sector credit growth data in 2003.

The trend represents a steep decline from 10.13 per cent in July 2024 before credit growth started falling steadily following the political transition in August that year.

Economists said that businesses postponed fresh investment decisions for months due to uncertainty over economic policies, a weak business environment, high inflation and continued global economic disruptions.

Although the February 12 national election delivered a decisive victory for the Bangladesh Nationalist Party, business confidence has yet to recover significantly.

Experts also said stress in the banking sector, tight monetary policy and aggressive government borrowing from banks further weakened credit flow to private businesses.

In its monetary policy statement for January–June 2026, Bangladesh Bank attributed the slowdown to tight liquidity conditions, weak demand for loans and increased government borrowing to finance the budget deficit.Bangladeshi Culture Course

Government borrowing has emerged as a major factor behind the credit squeeze.

During July–December of FY26, net government borrowing from the banking system reached Tk 98,000 crore, accounting for 99 per cent of the revised annual target.

Economists said excessive government borrowing absorbs a large portion of banks’ available funds, leaving less liquidity for businesses, particularly when many banks are already facing cash shortages.

The banking sector’s deteriorating financial health has also severely constrained lending capacity.

Defaulted loans stood at Tk 5.57 lakh crore at the end of December 2025, accounting for nearly one-third of total outstanding loans.

High levels of bad loans force banks to maintain large provisions against potential losses, reducing both profitability and their ability to issue fresh loans.

At the same time, high borrowing costs have discouraged businesses from taking new loans.

Bangladesh Bank’s policy interest rate currently stands at 10 per cent, while commercial lending rates in many cases have climbed close to 15 per cent.Politics

Such elevated rates have made borrowing increasingly expensive, particularly for small and medium-sized enterprises that depend heavily on bank financing for operations and expansion.

The impact of weak credit growth is already visible across the broader economy.

Imports of capital machinery have declined, indicating slower industrial expansion, while many factories are reportedly operating below capacity because of weak demand and limited access to working capital.

Lower private investment has also reduced money circulation in the economy, slowing business activities and limiting employment growth.

Bangladesh Bank has set a private sector credit growth target of 8.5 per cent for the second half of FY26, but economists said the current trend suggests the target may be difficult to achieve.

Staff Correspondent 20 May, 2026, 23:28

A file photo shows a man counting taka notes in the capital. | New Age photo

Private sector credit growth in Bangladesh fell to a historic low of 4.72 per cent in March 2026, reflecting sluggish business activities, weak investment appetite and continued stress across the economy.

According to data from Bangladesh Bank, private sector credit growth declined sharply 6.03 per cent in both January and February and 6.1 per cent in December, extending the prolonged slowdown in bank lending to businesses.

The March figure marked the lowest level in Bangladesh Bank’s recorded history since it began compiling private sector credit growth data in 2003.

The trend represents a steep decline from 10.13 per cent in July 2024 before credit growth started falling steadily following the political transition in August that year.

Economists said that businesses postponed fresh investment decisions for months due to uncertainty over economic policies, a weak business environment, high inflation and continued global economic disruptions.

Although the February 12 national election delivered a decisive victory for the Bangladesh Nationalist Party, business confidence has yet to recover significantly.

Experts also said stress in the banking sector, tight monetary policy and aggressive government borrowing from banks further weakened credit flow to private businesses.

In its monetary policy statement for January–June 2026, Bangladesh Bank attributed the slowdown to tight liquidity conditions, weak demand for loans and increased government borrowing to finance the budget deficit.Bangladeshi Culture Course

Government borrowing has emerged as a major factor behind the credit squeeze.

During July–December of FY26, net government borrowing from the banking system reached Tk 98,000 crore, accounting for 99 per cent of the revised annual target.

Economists said excessive government borrowing absorbs a large portion of banks’ available funds, leaving less liquidity for businesses, particularly when many banks are already facing cash shortages.

The banking sector’s deteriorating financial health has also severely constrained lending capacity.

Defaulted loans stood at Tk 5.57 lakh crore at the end of December 2025, accounting for nearly one-third of total outstanding loans.

High levels of bad loans force banks to maintain large provisions against potential losses, reducing both profitability and their ability to issue fresh loans.

At the same time, high borrowing costs have discouraged businesses from taking new loans.

Bangladesh Bank’s policy interest rate currently stands at 10 per cent, while commercial lending rates in many cases have climbed close to 15 per cent.Politics

Such elevated rates have made borrowing increasingly expensive, particularly for small and medium-sized enterprises that depend heavily on bank financing for operations and expansion.

The impact of weak credit growth is already visible across the broader economy.

Imports of capital machinery have declined, indicating slower industrial expansion, while many factories are reportedly operating below capacity because of weak demand and limited access to working capital.

Lower private investment has also reduced money circulation in the economy, slowing business activities and limiting employment growth.

Bangladesh Bank has set a private sector credit growth target of 8.5 per cent for the second half of FY26, but economists said the current trend suggests the target may be difficult to achieve.