Bangladesh Defense

Bangladesh DefenseSaif

Senior Member

- Jan 24, 2024

- 20,358

- 9,555

- Nation

- Residence

- Axis Group

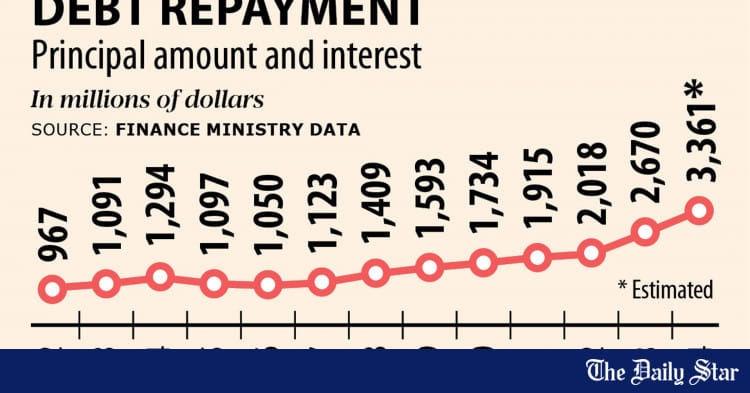

Budget For Fy25: 53pc rise in allocation for debt servicing

The government’s allocation to repay foreign debts may reach Tk 57,000 crore in the next budget, a 53 percent rise from the current year, putting further pressure on the country’s dwindling foreign currency reserves.

Budget For Fy25: 53pc rise in allocation for debt servicing

Spiralling amount will put strain on reserves, say experts

The government's allocation to repay foreign debts may reach Tk 57,000 crore in the next budget, a 53 percent rise from the current year, putting further pressure on the country's dwindling foreign currency reserves.

The interest payments for increasing levels of foreign loans in recent years and the tumbling value of the taka against the US dollar have forced the government to set aside more for debt servicing.

Allocation for foreign debt repayment has been Tk 37,076 crore in the current fiscal year, according to the finance ministry.

To read the rest of the news, please click on the link above.

Spiralling amount will put strain on reserves, say experts

The government's allocation to repay foreign debts may reach Tk 57,000 crore in the next budget, a 53 percent rise from the current year, putting further pressure on the country's dwindling foreign currency reserves.

The interest payments for increasing levels of foreign loans in recent years and the tumbling value of the taka against the US dollar have forced the government to set aside more for debt servicing.

Allocation for foreign debt repayment has been Tk 37,076 crore in the current fiscal year, according to the finance ministry.

To read the rest of the news, please click on the link above.