Bangladesh Defense

Bangladesh DefenseSaif

Senior Member

- Jan 24, 2024

- 20,305

- 9,554

- Nation

- Residence

- Axis Group

Monetary policy likely in last week of January

Bangladesh Bank will soon announce its monetary policy for the second half of the ongoing fiscal year (2024-25) with the aim of addressing several economic challenges plaguing the country.

Monetary policy likely in last week of January

Bangladesh Bank will soon announce its monetary policy for the second half of the ongoing fiscal year (2024-25) with the aim of addressing several economic challenges plaguing the country.

Sources at the central bank confirmed that the next monetary policy is being formulated, and that Governor Ahsan H Mansur will likely declare it by the last week of January.

This will be the first monetary policy announced by Mansur since he became governor of Bangladesh Bank following the political changeover on August 5.

As part of its efforts, the central bank has invited all interested individuals and institutions to send their suggestions, opinions, and feedback regarding potential policy measures by January 15.

Additionally, the monetary policy department of Bangladesh Bank will hold meetings with internal and external stakeholders as well as economists from January 12.

As part of its efforts, the central bank has invited all interested individuals and institutions to send their suggestions and feedback

But beforehand, the monetary policy department will hold a meeting with its executive directors and other senior officials at the central bank headquarters that same day to take their suggestions.

The department will then hold a discussion with the country's leading research organisations on January 14 on potential policy measures.

The organisations include the Bangladesh Institute of Development Studies, Policy Research Institute of Bangladesh and South Asian Network on Economic Modelling.

The Institute for Inclusive Finance and Development, Centre for Policy Dialogue, Research and Policy Integration for Development, reputed economists, bankers, businesspeople, and journalists will also attend the event at Lakeshore Hotel in Gulshan, Dhaka.

The central bank committee forming the monetary policy will ultimately summarise the observations from various quarters regarding its goals and format, including measures for regulating currency and lending rates, before finalising it on January 20.

Then on January 22, the board of directors of Bangladesh Bank will approve the policy and set a date for announcing it to the public.

Inflation in Bangladesh has been hovering above 9 percent since March 2023, with the central bank's existing contractionary monetary policy yet to cool consumer prices.

Bangladesh Bank has hiked the policy rate several times to 10 percent since then. The policy rate is the interest rate at which commercial banks borrow from the central bank.

But in December of the just concluded calendar year, inflation had eased slightly to 10.89 percent from 11.38 percent the previous month, according to the Bangladesh Bureau of Statistics (BBS).

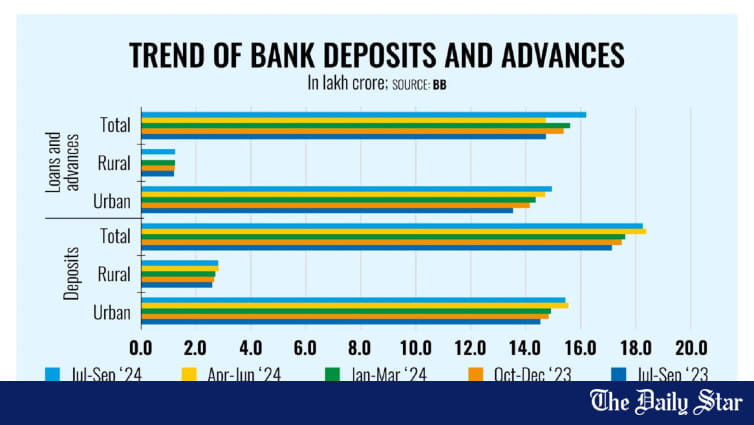

Other than inflationary pressure, the overall economy has been facing uncertainties ever since the fall of the Awami League government on August 5, as reflected in private sector credit growth.

In November last year, private sector credit growth fell to a three-and-a-half-year low of 7.66 percent, with the previous lowest being 7.55 percent in May 2021.

The volume of defaulted loans reached a gargantuan Tk 2,84,977 crore as of September last year, with some banks becoming unable to provide fresh loans amid a subsequent liquidity crunch.

However, the foreign exchange market has shown some flexibility as of late thanks to the recent uptick in incoming remittance.

Mustafa K Mujeri, executive director of the Institute for Inclusive Finance and Development, said hiking the policy rate to 10 percent has had no impact on alleviating the inflationary pressure.

"So, it would not be wise to raise the policy rate any further," he added.

Mujeri, also a former chief economist of Bangladesh Bank, said the central bank has one weapon for addressing inflation, which was the policy rate.

But increasing it now will only turn detrimental for the economy instead of tackling inflation, he added, citing how deposit and lending rates have risen for changes in the policy rate.

Mujeri suggested that other than augmenting its tight monetary stance, Bangladesh Bank has to find out the reasons for inflation in order to take effective measures to reduce it.

Bangladesh Bank will soon announce its monetary policy for the second half of the ongoing fiscal year (2024-25) with the aim of addressing several economic challenges plaguing the country.

Sources at the central bank confirmed that the next monetary policy is being formulated, and that Governor Ahsan H Mansur will likely declare it by the last week of January.

This will be the first monetary policy announced by Mansur since he became governor of Bangladesh Bank following the political changeover on August 5.

As part of its efforts, the central bank has invited all interested individuals and institutions to send their suggestions, opinions, and feedback regarding potential policy measures by January 15.

Additionally, the monetary policy department of Bangladesh Bank will hold meetings with internal and external stakeholders as well as economists from January 12.

As part of its efforts, the central bank has invited all interested individuals and institutions to send their suggestions and feedback

But beforehand, the monetary policy department will hold a meeting with its executive directors and other senior officials at the central bank headquarters that same day to take their suggestions.

The department will then hold a discussion with the country's leading research organisations on January 14 on potential policy measures.

The organisations include the Bangladesh Institute of Development Studies, Policy Research Institute of Bangladesh and South Asian Network on Economic Modelling.

The Institute for Inclusive Finance and Development, Centre for Policy Dialogue, Research and Policy Integration for Development, reputed economists, bankers, businesspeople, and journalists will also attend the event at Lakeshore Hotel in Gulshan, Dhaka.

The central bank committee forming the monetary policy will ultimately summarise the observations from various quarters regarding its goals and format, including measures for regulating currency and lending rates, before finalising it on January 20.

Then on January 22, the board of directors of Bangladesh Bank will approve the policy and set a date for announcing it to the public.

Inflation in Bangladesh has been hovering above 9 percent since March 2023, with the central bank's existing contractionary monetary policy yet to cool consumer prices.

Bangladesh Bank has hiked the policy rate several times to 10 percent since then. The policy rate is the interest rate at which commercial banks borrow from the central bank.

But in December of the just concluded calendar year, inflation had eased slightly to 10.89 percent from 11.38 percent the previous month, according to the Bangladesh Bureau of Statistics (BBS).

Other than inflationary pressure, the overall economy has been facing uncertainties ever since the fall of the Awami League government on August 5, as reflected in private sector credit growth.

In November last year, private sector credit growth fell to a three-and-a-half-year low of 7.66 percent, with the previous lowest being 7.55 percent in May 2021.

The volume of defaulted loans reached a gargantuan Tk 2,84,977 crore as of September last year, with some banks becoming unable to provide fresh loans amid a subsequent liquidity crunch.

However, the foreign exchange market has shown some flexibility as of late thanks to the recent uptick in incoming remittance.

Mustafa K Mujeri, executive director of the Institute for Inclusive Finance and Development, said hiking the policy rate to 10 percent has had no impact on alleviating the inflationary pressure.

"So, it would not be wise to raise the policy rate any further," he added.

Mujeri, also a former chief economist of Bangladesh Bank, said the central bank has one weapon for addressing inflation, which was the policy rate.

But increasing it now will only turn detrimental for the economy instead of tackling inflation, he added, citing how deposit and lending rates have risen for changes in the policy rate.

Mujeri suggested that other than augmenting its tight monetary stance, Bangladesh Bank has to find out the reasons for inflation in order to take effective measures to reduce it.