Bangladesh Defense

Bangladesh DefenseSaif

Senior Member

- Jan 24, 2024

- 20,457

- 9,566

- Nation

- Residence

- Axis Group

Govt to borrow 20pc higher from savings tools, 8pc more from banks

With an upscale new budget coming in few days now, the government targets borrowing 8.0-percent higher from the banking sector and 20-percent bigger from savings schemes to finance deficit amid unpromising revenue-earning prospects, officials say. According to Finance Division sources, in th

Govt to borrow 20pc higher from savings tools, 8pc more from banks

Possible failure of overrated revenue-target could lead to even overshooting of borrowing targets: Finance officials

Syful Islam

Published :

Jun 08, 2026 00:22

Updated :

Jun 08, 2026 00:22

With an upscale new budget coming in few days now, the government targets borrowing 8.0-percent higher from the banking sector and 20-percent bigger from savings schemes to finance deficit amid unpromising revenue-earning prospects, officials say.

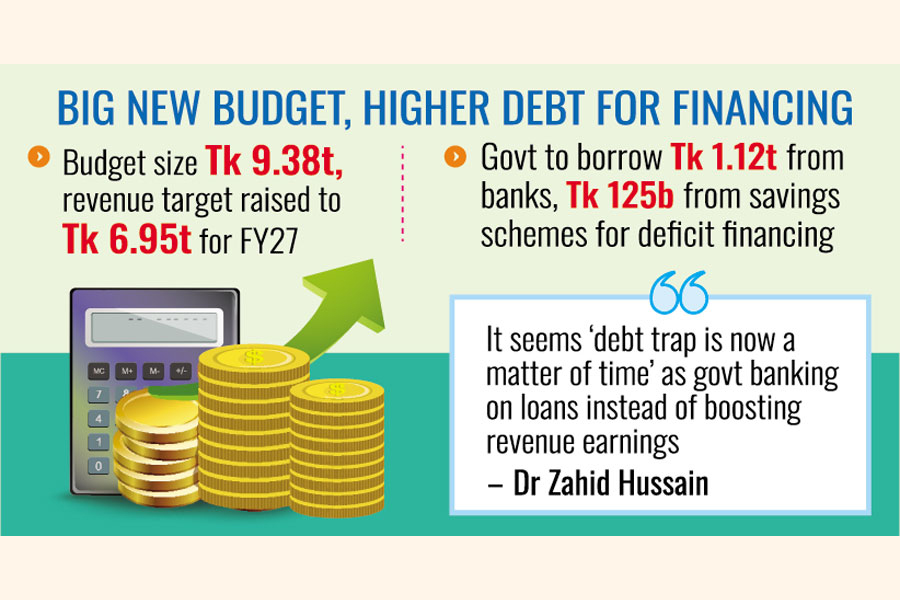

According to Finance Division sources, in the next fiscal year, the government plans to borrow some Tk 1.12 trillion from banks compared to current year's budgetary target of Tk 1.04 trillion.

Data show that until May 10, the government had actually borrowed Tk 1.95 trillion from the banking sector to meet its needs.

Also, the government is targeting to borrow some Tk 150 billion from the national savings schemes to help finance the Tk 9.38-trillion largest-ever fiscal budget in Bangladesh.

In the outgoing fiscal year, the government had targeted borrowing Tk 125 billion from national savings schemes. However, due to selling pressure from the buyers, the government's net selling of savings instruments fell into negative territory by Tk 5.55 billion until February last.

Officials say that as the government is making a large-size budget without confirming adequate sources of earnings, it will have no option but to raise dependence on the banking sector to meet its financial needs.

In the next year's budget, the government is setting a target of collecting Tk 6.95 trillion as revenues, compared to its highest revenue collection in the recent past amounting to Tk 4.09 trillion.

The finance officials say the National Board of Revenue (NBR) alone is going to be given a target to collect Tk 6.04 trillion, higher by Tk 2.43 trillion than its previous records in revenue mobilisation.

So, they say, as revenue collection will fall short of its target and foreign fund flow is not promising in the coming year, government's net bank borrowings will mount in the next fiscal year, surpassing the target.

Dr Zahid Hussain, a former lead economist at the World Bank's Dhaka office, says it seems that "debt trap is now a matter of time" as the government is increasingly depending on loans instead of enhancing revenue earnings.

"The money the government is borrowing from the banks is being used for meeting its operational needs instead of using them in productive sectors," the economist notes.

Thus, he adds, the government's debt burden is increasing day by day.

Because, he says, the government will have to return the money with interest.

Mr Hussain also makes a point that high government borrowing from banking sector lessens fund flow for private-sector investment, thus lowering employment growth that ultimately impacts overall economic growth in the country.

Possible failure of overrated revenue-target could lead to even overshooting of borrowing targets: Finance officials

Syful Islam

Published :

Jun 08, 2026 00:22

Updated :

Jun 08, 2026 00:22

With an upscale new budget coming in few days now, the government targets borrowing 8.0-percent higher from the banking sector and 20-percent bigger from savings schemes to finance deficit amid unpromising revenue-earning prospects, officials say.

According to Finance Division sources, in the next fiscal year, the government plans to borrow some Tk 1.12 trillion from banks compared to current year's budgetary target of Tk 1.04 trillion.

Data show that until May 10, the government had actually borrowed Tk 1.95 trillion from the banking sector to meet its needs.

Also, the government is targeting to borrow some Tk 150 billion from the national savings schemes to help finance the Tk 9.38-trillion largest-ever fiscal budget in Bangladesh.

In the outgoing fiscal year, the government had targeted borrowing Tk 125 billion from national savings schemes. However, due to selling pressure from the buyers, the government's net selling of savings instruments fell into negative territory by Tk 5.55 billion until February last.

Officials say that as the government is making a large-size budget without confirming adequate sources of earnings, it will have no option but to raise dependence on the banking sector to meet its financial needs.

In the next year's budget, the government is setting a target of collecting Tk 6.95 trillion as revenues, compared to its highest revenue collection in the recent past amounting to Tk 4.09 trillion.

The finance officials say the National Board of Revenue (NBR) alone is going to be given a target to collect Tk 6.04 trillion, higher by Tk 2.43 trillion than its previous records in revenue mobilisation.

So, they say, as revenue collection will fall short of its target and foreign fund flow is not promising in the coming year, government's net bank borrowings will mount in the next fiscal year, surpassing the target.

Dr Zahid Hussain, a former lead economist at the World Bank's Dhaka office, says it seems that "debt trap is now a matter of time" as the government is increasingly depending on loans instead of enhancing revenue earnings.

"The money the government is borrowing from the banks is being used for meeting its operational needs instead of using them in productive sectors," the economist notes.

Thus, he adds, the government's debt burden is increasing day by day.

Because, he says, the government will have to return the money with interest.

Mr Hussain also makes a point that high government borrowing from banking sector lessens fund flow for private-sector investment, thus lowering employment growth that ultimately impacts overall economic growth in the country.