Bangladesh Defense

Bangladesh DefenseSaif

Senior Member

- Jan 24, 2024

- 20,500

- 9,589

- Nation

- Residence

- Axis Group

Can Bangladesh finally fix its NPL problem?

Bangladesh Bank has unveiled an 18-month roadmap to tackle mounting non-performing loans (NPLs) and restore banking stability

Can Bangladesh finally fix its NPL problem?

Mamun Rashid

Bangladesh Bank has unveiled an 18-month roadmap to tackle mounting non-performing loans (NPLs) and restore banking stability. The plan combines stronger supervision, loan restructuring, faster recovery of distressed assets, legal reforms, capital restoration, and the new Bank Resolution and Deposit Protection Acts. It also introduces a much-debated one-time settlement scheme, under which borrowers repay only the principal while accumulated interest may be fully waived.

The announcement has drawn cautious optimism, but it revives a familiar question: is this a genuine break from the past, or another attempt to defer a deeper problem?

Our banking history offers reason for caution. Over the past decade, policymakers have leaned repeatedly on rescheduling, forbearance, and special repayment or restructuring facilities to contain defaults. In 2019, the then finance minister, an accountant, pledged that NPLs would not rise "by even a single penny".

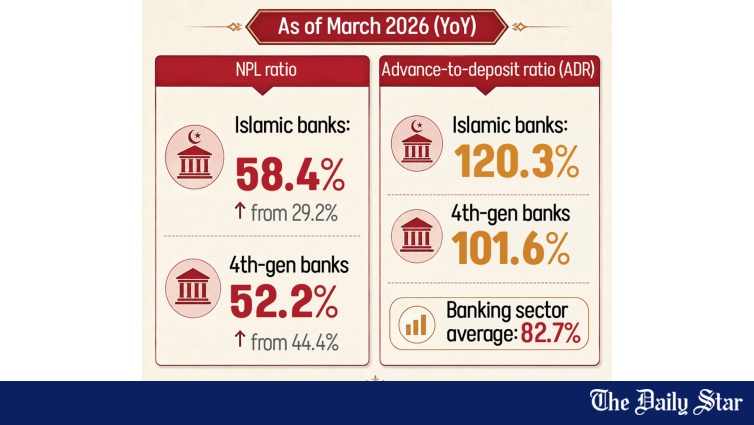

Instead, they climbed to nearly Tk 5.9 lakh crore – almost a third of total outstanding loans. If we include the written-off amount, the number would be much higher. Rather than resolving the crisis, successive policies largely delayed the recognition of losses and masked the true health of banks.

Banking crises rarely emerge overnight. They accumulate from weak governance, political interference, and poor credit discipline. When borrowers expect endless restructuring regardless of repayment behaviour, financial discipline erodes; when banks cannot enforce prudent lending, bad loans mature into a systemic risk.

The 2024 political transition marked an important shift, as Bangladesh Bank initiated Asset Quality Reviews (AQRs), exposed troubled banks’ true condition, identified capital shortfalls, and began exploring consolidation. The new roadmap appears to build on those reforms rather than reverse them.

The most debated element is the complete interest waiver. There is some logic to it – not every defaulter is wilful, and many businesses have struggled through economic shocks, rising energy costs, and financing costs. A realistic path back into the formal system could revive recovery and productive investment.

Yet a question remains: banks mostly lend depositors’ savings, apart from their meagre equity. If interest income is waived, who absorbs the loss – shareholders, depositors, or taxpayers? If weak banks eventually need recapitalisation, today’s relief becomes tomorrow’s fiscal burden. Cleaning up balance sheets is necessary, but not at the cost of long-term financial stability.

International experience shows successful reform never rests on a single instrument. After the Asian financial crisis, South Korea’s asset management company (KAMCO) purchased distressed loans, restructured viable assets, and restored confidence. Malaysia’s Danaharta played a similar role, acquiring troubled assets and disposing of unviable ones under a strong legal framework. Both governments recovered a substantial share of the public resources deployed. Carlyle, from the USA, played a significant role in cleaning up toxic assets in some Chinese banks after the Asian meltdown.

Not every such initiative has succeeded. Similar efforts in Indonesia and Nigeria were undermined by political interference and drawn-out legal processes. The lesson is simple: an asset management company is no cure by itself. It works only within a broader reform agenda – independent supervision, efficient courts, transparent governance, and the will to pursue influential defaulters without favour.

This is directly relevant as our central bank moves to establish its own AMC. Its success will hinge less on legal creation than on operational independence and freedom from political interference.

Encouragingly, the ADB, IMF, and World Bank have tied support to measurable improvements in banking governance. External pressure cannot replace domestic leadership, but it does raise the cost of complacency.

Bangladesh’s banking sector stands at a critical juncture. Success will depend not on ambition but on the credibility of execution. If political considerations override financial discipline, this too will join a long list of missed opportunities. But if policymakers recognise losses honestly and enforce accountability without exception, this roadmap could yet become the country’s most meaningful banking reform in decades.

Reducing NPLs is not merely about repairing balance sheets; it is about restoring public trust, protecting depositors’ savings, and safeguarding long-term growth. The real test will not be whether reported NPLs fall over the next 18 months, but whether the institutional failures behind the crisis are finally addressed.

Mamun Rashid is an economic analyst and chairman at Financial Excellence Ltd.

Mamun Rashid

Bangladesh Bank has unveiled an 18-month roadmap to tackle mounting non-performing loans (NPLs) and restore banking stability. The plan combines stronger supervision, loan restructuring, faster recovery of distressed assets, legal reforms, capital restoration, and the new Bank Resolution and Deposit Protection Acts. It also introduces a much-debated one-time settlement scheme, under which borrowers repay only the principal while accumulated interest may be fully waived.

The announcement has drawn cautious optimism, but it revives a familiar question: is this a genuine break from the past, or another attempt to defer a deeper problem?

Our banking history offers reason for caution. Over the past decade, policymakers have leaned repeatedly on rescheduling, forbearance, and special repayment or restructuring facilities to contain defaults. In 2019, the then finance minister, an accountant, pledged that NPLs would not rise "by even a single penny".

Instead, they climbed to nearly Tk 5.9 lakh crore – almost a third of total outstanding loans. If we include the written-off amount, the number would be much higher. Rather than resolving the crisis, successive policies largely delayed the recognition of losses and masked the true health of banks.

Banking crises rarely emerge overnight. They accumulate from weak governance, political interference, and poor credit discipline. When borrowers expect endless restructuring regardless of repayment behaviour, financial discipline erodes; when banks cannot enforce prudent lending, bad loans mature into a systemic risk.

The 2024 political transition marked an important shift, as Bangladesh Bank initiated Asset Quality Reviews (AQRs), exposed troubled banks’ true condition, identified capital shortfalls, and began exploring consolidation. The new roadmap appears to build on those reforms rather than reverse them.

The most debated element is the complete interest waiver. There is some logic to it – not every defaulter is wilful, and many businesses have struggled through economic shocks, rising energy costs, and financing costs. A realistic path back into the formal system could revive recovery and productive investment.

Yet a question remains: banks mostly lend depositors’ savings, apart from their meagre equity. If interest income is waived, who absorbs the loss – shareholders, depositors, or taxpayers? If weak banks eventually need recapitalisation, today’s relief becomes tomorrow’s fiscal burden. Cleaning up balance sheets is necessary, but not at the cost of long-term financial stability.

International experience shows successful reform never rests on a single instrument. After the Asian financial crisis, South Korea’s asset management company (KAMCO) purchased distressed loans, restructured viable assets, and restored confidence. Malaysia’s Danaharta played a similar role, acquiring troubled assets and disposing of unviable ones under a strong legal framework. Both governments recovered a substantial share of the public resources deployed. Carlyle, from the USA, played a significant role in cleaning up toxic assets in some Chinese banks after the Asian meltdown.

Not every such initiative has succeeded. Similar efforts in Indonesia and Nigeria were undermined by political interference and drawn-out legal processes. The lesson is simple: an asset management company is no cure by itself. It works only within a broader reform agenda – independent supervision, efficient courts, transparent governance, and the will to pursue influential defaulters without favour.

This is directly relevant as our central bank moves to establish its own AMC. Its success will hinge less on legal creation than on operational independence and freedom from political interference.

Encouragingly, the ADB, IMF, and World Bank have tied support to measurable improvements in banking governance. External pressure cannot replace domestic leadership, but it does raise the cost of complacency.

Bangladesh’s banking sector stands at a critical juncture. Success will depend not on ambition but on the credibility of execution. If political considerations override financial discipline, this too will join a long list of missed opportunities. But if policymakers recognise losses honestly and enforce accountability without exception, this roadmap could yet become the country’s most meaningful banking reform in decades.

Reducing NPLs is not merely about repairing balance sheets; it is about restoring public trust, protecting depositors’ savings, and safeguarding long-term growth. The real test will not be whether reported NPLs fall over the next 18 months, but whether the institutional failures behind the crisis are finally addressed.

Mamun Rashid is an economic analyst and chairman at Financial Excellence Ltd.