Bangladesh Defense

Bangladesh DefenseSaif

Senior Member

- Jan 24, 2024

- 20,562

- 9,607

- Nation

- Residence

- Axis Group

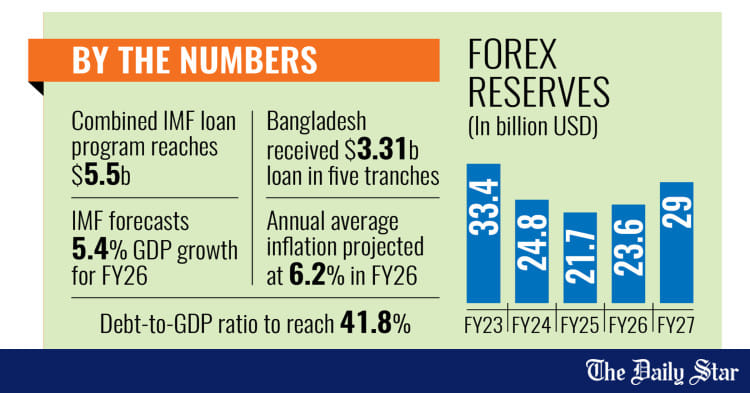

$400m more comes from AIIB

Assistance worth US$400 million is forthcoming from the Asian Infrastructure Investment Bank (AIIB) in a latest flow of foreign aid for bankrolling Bangladesh's budgetary programmes--this one for climate-centric reforms. This amount comes under a credit deal signed Monday in Dhaka between Econom

Budget support

$400m more comes from AIIB

Reforms regarding climate resilience in focus

FE REPORT

Published :

Jun 24, 2025 00:55

Updated :

Jun 24, 2025 00:55

Assistance worth US$400 million is forthcoming from the Asian Infrastructure Investment Bank (AIIB) in a latest flow of foreign aid for bankrolling Bangladesh's budgetary programmes--this one for climate-centric reforms.

This amount comes under a credit deal signed Monday in Dhaka between Economic Relations Division (ERD) under the Ministry of Finance (MoF) and the China-based AIIB.

Additional Secretary of the ERD Mirana Mahrukh and the AIIB Acting Chief Adviser Rajat Misra inked the deal. Under terms of funding laid down in the 'Climate Resilient Inclusive Development Programme-Subprogramme-2', Bangladesh has to conduct different climate-related reforms, officials said.

The AIIB's $400-million budget support would be the co-financing with the Asian Development Bank (ADB) where the Manila-based lender provided a $400 million to help Bangladesh enhance its resilience against climate impacts, cut emissions in climate-critical sectors, and promote inclusive development.

With AIIB and ADB's financial supports, the Ministry of Finance (MoF) would establish "environment for climate priorities across the ministries, facilitate climate-adaptation priorities, and accelerate climate-change-mitigation actions".

Meanwhile, the World Bank on June 21 confirmed US$500 million worth of budget support and the Asian Development Bank another $500 million on June 20.

The $500-million budget support from the ADB would be utilised to stabilise and reform the banking sector by strengthening regulatory supervision, corporate governance, asset quality, and stability.

The AIIB will charge SOFR-plus a variable spread and a 0.25-percent front-end fee for the $400 million loan confirmed Monday, ERD officials said.

The maturity of the loan will be 35 years with a grace period of five years.

Under the 'Climate Resilient Inclusive Development Program- Subprogramme-1' last year, the AIIB also provided another $400 million to Bangladesh in budget support for implementing some climate-related reforms.

$400m more comes from AIIB

Reforms regarding climate resilience in focus

FE REPORT

Published :

Jun 24, 2025 00:55

Updated :

Jun 24, 2025 00:55

Assistance worth US$400 million is forthcoming from the Asian Infrastructure Investment Bank (AIIB) in a latest flow of foreign aid for bankrolling Bangladesh's budgetary programmes--this one for climate-centric reforms.

This amount comes under a credit deal signed Monday in Dhaka between Economic Relations Division (ERD) under the Ministry of Finance (MoF) and the China-based AIIB.

Additional Secretary of the ERD Mirana Mahrukh and the AIIB Acting Chief Adviser Rajat Misra inked the deal. Under terms of funding laid down in the 'Climate Resilient Inclusive Development Programme-Subprogramme-2', Bangladesh has to conduct different climate-related reforms, officials said.

The AIIB's $400-million budget support would be the co-financing with the Asian Development Bank (ADB) where the Manila-based lender provided a $400 million to help Bangladesh enhance its resilience against climate impacts, cut emissions in climate-critical sectors, and promote inclusive development.

With AIIB and ADB's financial supports, the Ministry of Finance (MoF) would establish "environment for climate priorities across the ministries, facilitate climate-adaptation priorities, and accelerate climate-change-mitigation actions".

Meanwhile, the World Bank on June 21 confirmed US$500 million worth of budget support and the Asian Development Bank another $500 million on June 20.

The $500-million budget support from the ADB would be utilised to stabilise and reform the banking sector by strengthening regulatory supervision, corporate governance, asset quality, and stability.

The AIIB will charge SOFR-plus a variable spread and a 0.25-percent front-end fee for the $400 million loan confirmed Monday, ERD officials said.

The maturity of the loan will be 35 years with a grace period of five years.

Under the 'Climate Resilient Inclusive Development Program- Subprogramme-1' last year, the AIIB also provided another $400 million to Bangladesh in budget support for implementing some climate-related reforms.