Bangladesh Defense

Bangladesh DefenseSaif

Senior Member

- Jan 24, 2024

- 20,536

- 9,606

- Nation

- Residence

- Axis Group

Macroeconomic management matters

The danger of macroeconomic mismanagement was aptly highlighted by Paul Krugman (1994) and William Easterly (2001), who cautioned that inefficient resource allocation can undermine the gains from openness and investment, leading to economic stagnation even amid high levels of public spending. Soun

Macroeconomic management matters

Bangladesh's growth story is unsustainable indefinitely otherwise

N N Tarun Chakravorty

Published :

Dec 31, 2025 22:59

Updated :

Dec 31, 2025 23:14

The danger of macroeconomic mismanagement was aptly highlighted by Paul Krugman (1994) and William Easterly (2001), who cautioned that inefficient resource allocation can undermine the gains from openness and investment, leading to economic stagnation even amid high levels of public spending.

Sound macroeconomic management, which involves prudent fiscal, monetary, and exchange rate policies, builds the foundation upon which growth can occur. What are these sound macroeconomic indicators? Stable prices, manageable debt, and a credible currency. Before domestic and foreign investors plan, invest, and take risks, they look at this stability. In contrast, high inflation, fiscal indiscipline, or currency instability shoo away investor and thus erode savings and distort incentives.

Bangladesh has been experiencing chronic fiscal deficits financed by borrowing from the central bank, have contributed to inflationary pressures. The government's policy of extending subsidies, granting tax exemptions, and allowing non-performing loans (NPLs) to persist in state-owned banks has weakened fiscal discipline and constrained private investment.

Good macro management ensures that resources flow to productive sectors rather than being wasted on rent-seeking or politically motivated projects. Fiscal policy must prioritise infrastructure, education, and innovation over populist subsidies or politically driven spending. Monetary policy must support productive investment by maintaining real interest rates that encourage saving and discourage speculative activities.

In recent times, Sri Lanka appeared to be an example of macroeconomic mismanagement. Sri Lanka's government payroll has expanded dramatically over the decades. Many of these positions were created for political patronage rather than productivity. This distorted resource allocation has diverted fiscal resources from capital investment-in infrastructure, technology, and industrial upgrading-to recurrent expenditures like salaries and pensions.

The Rajapaksa government focused heavily on large-scale infrastructure projects-ports, airports, and stadiums-many financed through Chinese loans. It appeared to be fancy project which was a sheer populist move. This move increased public debt without generating proportionate growth, crowding out more productive investments such as export diversification and SME development. Sri Lanka's chronic fiscal deficits and mounting debt service-largely due to unproductive expenditure-culminated in the 2022 debt crisis, which in turn caused huge public uproar and ultimately, the fall of the government.

Bangladesh's case is slightly different from Sri Lanka's regarding big projects. Bangladesh's big projects are not unproductive meaning that they exerted a positive impact on economic activities leading to higher growth. Secondly, its public debt remained moderate (around 40 per cent of GDP) and external debt was largely concessional, keeping debt service manageable while Sri Lanka's debt exceeded 120 per cent of GDP by 2022) and ultimately, sovereign default.

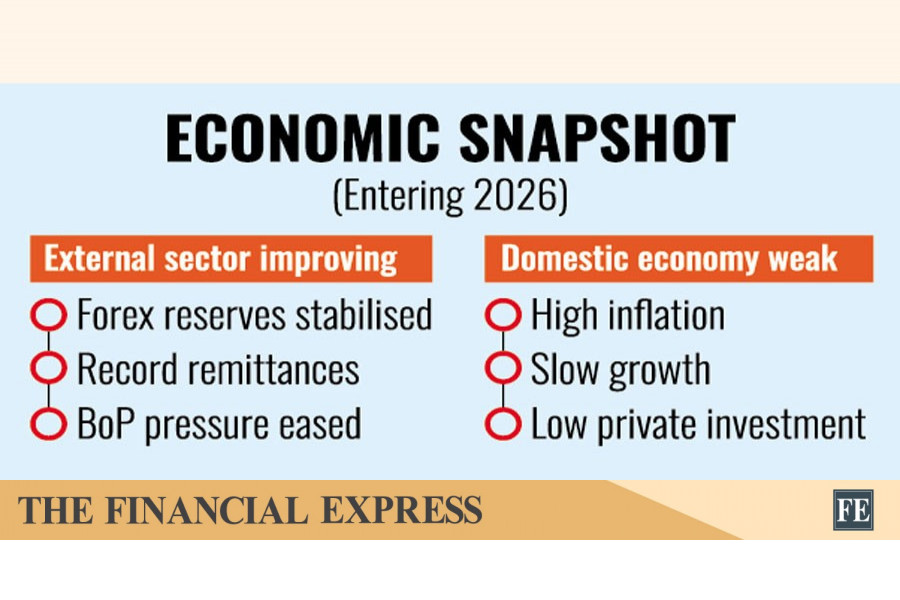

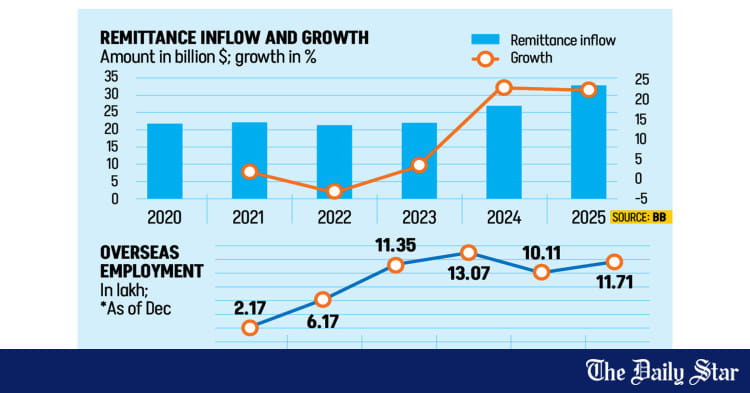

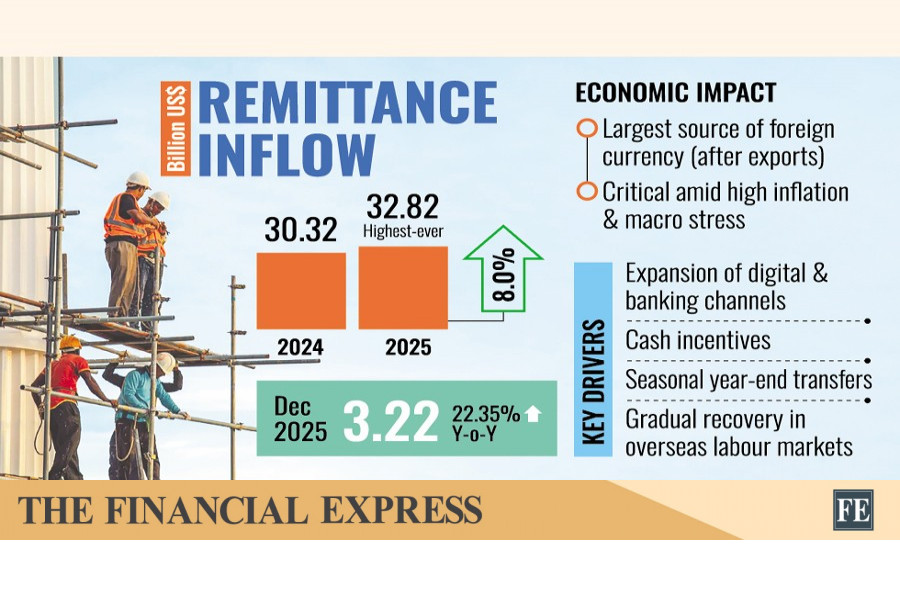

Bangladesh maintained relatively prudent fiscal policies for much of the past two decades. However, fiscal pressure has been rising in recent years due to mounting subsidies, inefficient state-owned enterprises, and revenue stagnation. Following the COVID-19 shock Sri Lanka went into a crisis triggered by foreign exchange depletion because its overreliance on tourism and remittances. But COVID-19 shock was relatively low Bangladesh as it historically enjoyed a robust current account surplus due to garment exports and remittance inflows, which was not much disrupted by COVID-19.

Sri Lanka's politically motivated currency overvaluation depleted reserves and crippled exports, while Bangladesh's managed float - marked by delayed adjustments and multiple exchange rates since 2022 - reflects a milder, yet increasingly risky, version of the same mismanagement.

Strong macro management means consistent policies, fiscal transparency, independent central banking, rule-based governance and institutional strength. All these are essential for gaining trust, attracting foreign direct investment (FDI) and aid. In Bangladesh the loss of central bank independence and intervention have undermined confidence in economic governance. The recent IMF program itself is a reminder of the cost of delayed adjustment and policy complacency.

Macroeconomic stability is not just about growth rates - it determines whether growth is inclusive and sustainable. In Bangladesh high inflation and fiscal mismanagement have been prevalent. High inflation, low tax-GDP ratio (less than 9 per cent of GDP),cuts in subsidies and allocation for safety nets and spending on health, education, and climate resilience have disproportionately hurt the poor, eroding real incomes and inequality. Fiscal mismanagement limits the state's ability to finance social safety nets and human capital development. These phenomena have prevented redistribution, public investment, and social protection. It has given rise in real poverty and inequality.

We all must keep in mind that good macroeconomic management is not just about balancing budgets or not a technocratic issue; it is deeply political and institutional. It reflects whether a government prioritises long-term national interest over short-term political gain. It's about balancing politics, institutions, and incentives. It creates the stability and confidence that allow entrepreneurship, innovation, and development to flourish.

We have the examples of countries like South Korea or Vietnam achieving sustained rapid growth precisely because they maintained fiscal prudence, export competitiveness, and policy credibility even under political transitions.

The World Bank, in its 2024 and 2025 updates for Bangladesh, has reiterated urgent monetary reform and introduction of a single-rate exchange regime for improving foreign-exchange reserves and taming inflation. It advised to raise revenue earnings (domestic resource mobilisation), so as to free up fiscal space for infrastructure and human-capital investment. It has highlighted the need for bold and urgent reforms particularly in the financial sector. At the moment, Bangladesh's fiscal deficit is around 4.5 per cent of GDP. The WB has projected continuing pressure unless fiscal consolidation, monetary discipline, and structural reforms take place.

As Nobel laureate Robert Solow (1956) showed, long-run growth depends not only on capital and labour but also on the efficiency with which resources are used-something that macroeconomic stability makes possible. Yet, efficiency is rarely discussed in Bangladesh's growth narrative. For decades, the economy has thrived on garments exports, remittances, and a demographic dividend, but this model-built on low-cost labour and export-led production-cannot sustain growth indefinitely. The next phase must focus on innovation-driven development, supported by disciplined macroeconomic management. Building efficiency demands credible institutions, fiscal prudence, and incentives that channel resources toward productive use-through better public finance and banking discipline, reduced corruption and red tape, and greater investment in skills and innovation.

Dr N N Tarun Chakravorty is professor of economics, IUB, and Editor-At-Large, South Asia Journal.

Bangladesh's growth story is unsustainable indefinitely otherwise

N N Tarun Chakravorty

Published :

Dec 31, 2025 22:59

Updated :

Dec 31, 2025 23:14

The danger of macroeconomic mismanagement was aptly highlighted by Paul Krugman (1994) and William Easterly (2001), who cautioned that inefficient resource allocation can undermine the gains from openness and investment, leading to economic stagnation even amid high levels of public spending.

Sound macroeconomic management, which involves prudent fiscal, monetary, and exchange rate policies, builds the foundation upon which growth can occur. What are these sound macroeconomic indicators? Stable prices, manageable debt, and a credible currency. Before domestic and foreign investors plan, invest, and take risks, they look at this stability. In contrast, high inflation, fiscal indiscipline, or currency instability shoo away investor and thus erode savings and distort incentives.

Bangladesh has been experiencing chronic fiscal deficits financed by borrowing from the central bank, have contributed to inflationary pressures. The government's policy of extending subsidies, granting tax exemptions, and allowing non-performing loans (NPLs) to persist in state-owned banks has weakened fiscal discipline and constrained private investment.

Good macro management ensures that resources flow to productive sectors rather than being wasted on rent-seeking or politically motivated projects. Fiscal policy must prioritise infrastructure, education, and innovation over populist subsidies or politically driven spending. Monetary policy must support productive investment by maintaining real interest rates that encourage saving and discourage speculative activities.

In recent times, Sri Lanka appeared to be an example of macroeconomic mismanagement. Sri Lanka's government payroll has expanded dramatically over the decades. Many of these positions were created for political patronage rather than productivity. This distorted resource allocation has diverted fiscal resources from capital investment-in infrastructure, technology, and industrial upgrading-to recurrent expenditures like salaries and pensions.

The Rajapaksa government focused heavily on large-scale infrastructure projects-ports, airports, and stadiums-many financed through Chinese loans. It appeared to be fancy project which was a sheer populist move. This move increased public debt without generating proportionate growth, crowding out more productive investments such as export diversification and SME development. Sri Lanka's chronic fiscal deficits and mounting debt service-largely due to unproductive expenditure-culminated in the 2022 debt crisis, which in turn caused huge public uproar and ultimately, the fall of the government.

Bangladesh's case is slightly different from Sri Lanka's regarding big projects. Bangladesh's big projects are not unproductive meaning that they exerted a positive impact on economic activities leading to higher growth. Secondly, its public debt remained moderate (around 40 per cent of GDP) and external debt was largely concessional, keeping debt service manageable while Sri Lanka's debt exceeded 120 per cent of GDP by 2022) and ultimately, sovereign default.

Bangladesh maintained relatively prudent fiscal policies for much of the past two decades. However, fiscal pressure has been rising in recent years due to mounting subsidies, inefficient state-owned enterprises, and revenue stagnation. Following the COVID-19 shock Sri Lanka went into a crisis triggered by foreign exchange depletion because its overreliance on tourism and remittances. But COVID-19 shock was relatively low Bangladesh as it historically enjoyed a robust current account surplus due to garment exports and remittance inflows, which was not much disrupted by COVID-19.

Sri Lanka's politically motivated currency overvaluation depleted reserves and crippled exports, while Bangladesh's managed float - marked by delayed adjustments and multiple exchange rates since 2022 - reflects a milder, yet increasingly risky, version of the same mismanagement.

Strong macro management means consistent policies, fiscal transparency, independent central banking, rule-based governance and institutional strength. All these are essential for gaining trust, attracting foreign direct investment (FDI) and aid. In Bangladesh the loss of central bank independence and intervention have undermined confidence in economic governance. The recent IMF program itself is a reminder of the cost of delayed adjustment and policy complacency.

Macroeconomic stability is not just about growth rates - it determines whether growth is inclusive and sustainable. In Bangladesh high inflation and fiscal mismanagement have been prevalent. High inflation, low tax-GDP ratio (less than 9 per cent of GDP),cuts in subsidies and allocation for safety nets and spending on health, education, and climate resilience have disproportionately hurt the poor, eroding real incomes and inequality. Fiscal mismanagement limits the state's ability to finance social safety nets and human capital development. These phenomena have prevented redistribution, public investment, and social protection. It has given rise in real poverty and inequality.

We all must keep in mind that good macroeconomic management is not just about balancing budgets or not a technocratic issue; it is deeply political and institutional. It reflects whether a government prioritises long-term national interest over short-term political gain. It's about balancing politics, institutions, and incentives. It creates the stability and confidence that allow entrepreneurship, innovation, and development to flourish.

We have the examples of countries like South Korea or Vietnam achieving sustained rapid growth precisely because they maintained fiscal prudence, export competitiveness, and policy credibility even under political transitions.

The World Bank, in its 2024 and 2025 updates for Bangladesh, has reiterated urgent monetary reform and introduction of a single-rate exchange regime for improving foreign-exchange reserves and taming inflation. It advised to raise revenue earnings (domestic resource mobilisation), so as to free up fiscal space for infrastructure and human-capital investment. It has highlighted the need for bold and urgent reforms particularly in the financial sector. At the moment, Bangladesh's fiscal deficit is around 4.5 per cent of GDP. The WB has projected continuing pressure unless fiscal consolidation, monetary discipline, and structural reforms take place.

As Nobel laureate Robert Solow (1956) showed, long-run growth depends not only on capital and labour but also on the efficiency with which resources are used-something that macroeconomic stability makes possible. Yet, efficiency is rarely discussed in Bangladesh's growth narrative. For decades, the economy has thrived on garments exports, remittances, and a demographic dividend, but this model-built on low-cost labour and export-led production-cannot sustain growth indefinitely. The next phase must focus on innovation-driven development, supported by disciplined macroeconomic management. Building efficiency demands credible institutions, fiscal prudence, and incentives that channel resources toward productive use-through better public finance and banking discipline, reduced corruption and red tape, and greater investment in skills and innovation.

Dr N N Tarun Chakravorty is professor of economics, IUB, and Editor-At-Large, South Asia Journal.