Bangladesh Defense

Bangladesh DefenseSaif

Senior Member

- Jan 24, 2024

- 20,156

- 9,518

- Nation

- Residence

- Axis Group

Elected govt to decide on BB autonomy: Finance adviser

Finance adviser Salehuddin Ahmed has said that sweeping amendments to the Bangladesh Bank Order, 1972 proposed by Bangladesh Bank governor Ahsan H Mansur during the tenure of the interim government will not be rational...

www.newagebd.net

www.newagebd.net

Elected govt to decide on BB autonomy: Finance adviser

Staff Correspondent 08 February, 2026, 00:10

Salehuddin Ahmed. | New Age file photo

Finance adviser Salehuddin Ahmed has said that sweeping amendments to the Bangladesh Bank Order, 1972 proposed by Bangladesh Bank governor Ahsan H Mansur during the tenure of the interim government will not be rational.

In a letter to Bangladesh Bank governor Ahsan H Mansur on February 5, Salehuddin welcomed the governor’s initiative to reinforce the central bank’s independence but cautioned that changes to such a core law should not be rushed without broad consultation and political legitimacy.

Bangladesh Bank governor Ahsan H Mansur had expressed the desire to pass the amendments before the interim government’s tenure ends at several programs.

Salehuddin said that he had examined the proposed amendments to the Bangladesh Bank Order, 1972, including provisions on the appointment and removal of top officials, enhancement of the governor’s status, changes to the board structure, expanded authority to create financial liabilities for the state, and safeguards against conflicts of interest.Bangladesh cultural tours

He stressed that the Bangladesh Bank Order is a foundational law governing the country’s central banking framework and that any amendment requires rigorous scrutiny of its justification.

He said that proposed changes should be reviewed in detail and discussed with key stakeholders, experts and relevant institutions before any decision is taken.

The adviser said that introducing extensive amendments to such a fundamental law during the interim government’s limited tenure would not be practical.

He suggested that a comprehensive review and revision of the order should be left to the next elected government, which would have a clearer mandate to undertake structural legal reforms.

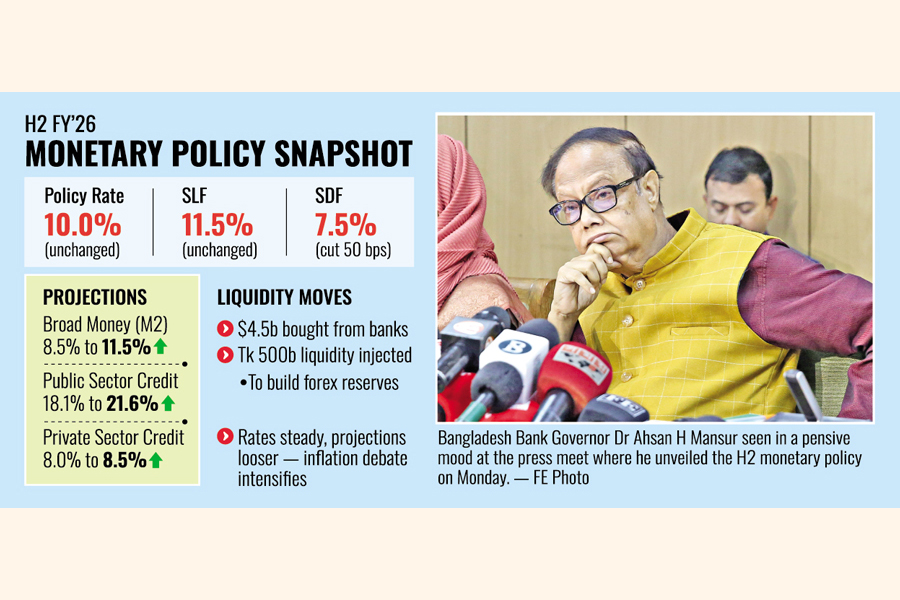

Governor Ahsan H Mansur has earlier told local media that without stronger legal independence, Bangladesh Bank would remain vulnerable to political pressure, weakening its ability to enforce discipline, address loan irregularities and ensure financial stability.

He has argued that autonomy is critical for restoring credibility in monetary policy and banking supervision.

Economists broadly agree that Bangladesh Bank needs greater independence but warn that autonomy must be matched with transparency, accountability and checks on concentrated power.

Staff Correspondent 08 February, 2026, 00:10

Salehuddin Ahmed. | New Age file photo

Finance adviser Salehuddin Ahmed has said that sweeping amendments to the Bangladesh Bank Order, 1972 proposed by Bangladesh Bank governor Ahsan H Mansur during the tenure of the interim government will not be rational.

In a letter to Bangladesh Bank governor Ahsan H Mansur on February 5, Salehuddin welcomed the governor’s initiative to reinforce the central bank’s independence but cautioned that changes to such a core law should not be rushed without broad consultation and political legitimacy.

Bangladesh Bank governor Ahsan H Mansur had expressed the desire to pass the amendments before the interim government’s tenure ends at several programs.

Salehuddin said that he had examined the proposed amendments to the Bangladesh Bank Order, 1972, including provisions on the appointment and removal of top officials, enhancement of the governor’s status, changes to the board structure, expanded authority to create financial liabilities for the state, and safeguards against conflicts of interest.Bangladesh cultural tours

He stressed that the Bangladesh Bank Order is a foundational law governing the country’s central banking framework and that any amendment requires rigorous scrutiny of its justification.

He said that proposed changes should be reviewed in detail and discussed with key stakeholders, experts and relevant institutions before any decision is taken.

The adviser said that introducing extensive amendments to such a fundamental law during the interim government’s limited tenure would not be practical.

He suggested that a comprehensive review and revision of the order should be left to the next elected government, which would have a clearer mandate to undertake structural legal reforms.

Governor Ahsan H Mansur has earlier told local media that without stronger legal independence, Bangladesh Bank would remain vulnerable to political pressure, weakening its ability to enforce discipline, address loan irregularities and ensure financial stability.

He has argued that autonomy is critical for restoring credibility in monetary policy and banking supervision.

Economists broadly agree that Bangladesh Bank needs greater independence but warn that autonomy must be matched with transparency, accountability and checks on concentrated power.