Bangladesh Defense

Bangladesh Defense- Jan 24, 2024

- 4,028

- 2,198

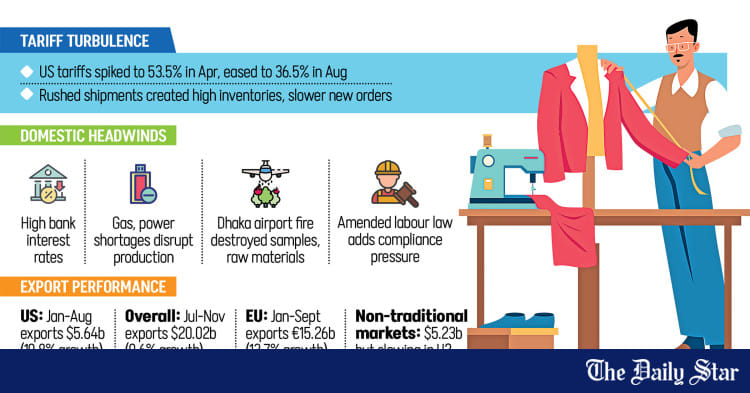

Bangladesh' RMG exports to USA, in absence of tariffs that affect Indian and Chinese exports have gone up around 18% which is as of last FY (post no. 399 above).

This will go up even more this FY.

However - as you said, knit sector is facing some problems due to Bank non-cooperation.

We also need to diversify exports, which is a crying need of the day. It is happening, but not fast enough.

This will go up even more this FY.

However - as you said, knit sector is facing some problems due to Bank non-cooperation.

We also need to diversify exports, which is a crying need of the day. It is happening, but not fast enough.