Bangladesh Defense

Bangladesh DefenseSaif

Senior Member

- Jan 24, 2024

- 20,562

- 9,607

- Nation

- Residence

- Axis Group

Nov Islamic banking up on remittances, investments

The Islamic banking sector in Bangladesh staged a significant comeback in November 2025, buoyed by a robust surge in inward remittances and a steady rise in Shariah-compliant investments. After a period of structural adjustments and governance reforms, the sector recorded double-digit growth in in

Nov Islamic banking up on remittances, investments

SAJIBUR RAHMAN

Published :

Jan 25, 2026 08:22

Updated :

Jan 25, 2026 08:22

The Islamic banking sector in Bangladesh staged a significant comeback in November 2025, buoyed by a robust surge in inward remittances and a steady rise in Shariah-compliant investments.

After a period of structural adjustments and governance reforms, the sector recorded double-digit growth in investments and total assets, indicating a restoration of depositor confidence, particularly among expatriates and rural savers.

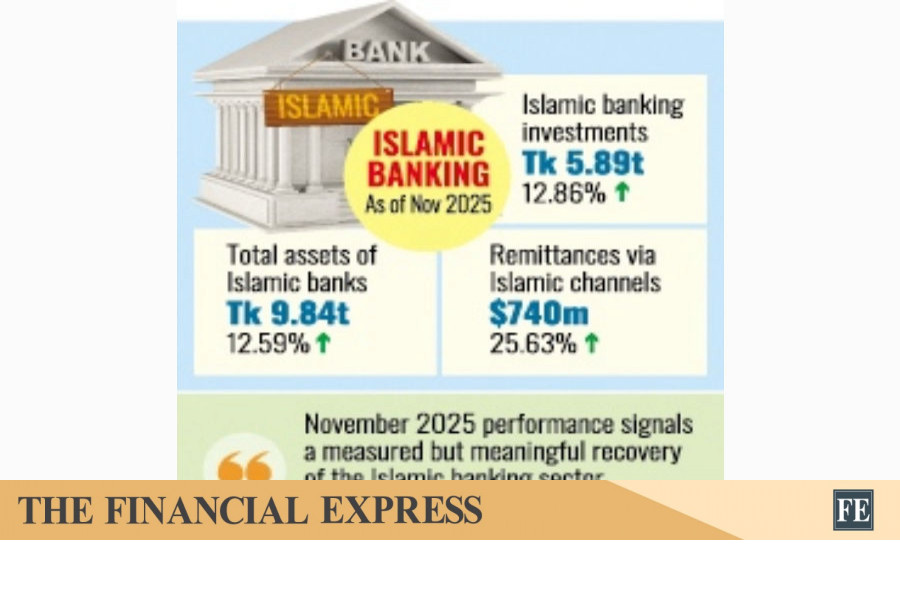

According to Bangladesh Bank (BB) data, the Islamic banking system recorded considerable growth in investments, rising 12.86 per cent to Tk 5.89 trillion in November 2025, up from Tk 5.21 trillion in the same month of the previous year.

While the conventional banking system also experienced growth -- rising from Tk 16.07 trillion to Tk 17.78 trillion -- its 10.60 per cent increase was slightly outpaced by Shariah-based lenders.

This expansion has solidified the Islamic sector's position, which now accounts for approximately one-fourth of total investment in the country's banking industry.

Total assets of Islamic banks saw a "robust growth" of 12.59 per cent, jumping from Tk 8.74 trillion to Tk 9.84 trillion during the period under review.

Perhaps the most striking highlight of the sector's performance is the recovery of its remittance share.

Remittances through Islamic channels surged from $472 million in November 2024 to $740 million in November 2025.

"The regained confidence of foreign workers in Islamic banks, likely due to improved management and tighter regulatory oversight, has been a primary driver for this 25.63 per cent jump in remittance share," said a senior central bank official.

In contrast, the trade sector showed more stability than growth.

Export proceeds via Islamic banks saw a slight decline of 4.41 per cent, standing at $668 million, while import payments marginally decreased 1.90 per cent to $1.04 billion.

Islamic banks continue to dominate the agent banking landscape, serving as a critical bridge for financial inclusion. Personal finance advice

They hold 54.58 per cent of total deposits in the agent banking arena. Deposits in this segment rose to Tk 261 billion in November 2025, marking a sharp 22.67 per cent year-on-year growth.

The BB report said full-fledged Islamic banks remain the primary drivers of the sector, sanctioning 91 per cent of all Islamic investments, while conventional banks operating through Islamic branches and windows contributed the remaining 9 per cent.

Industry experts suggest that while the sector has shown resilience, maintaining this momentum will require continued focus on governance and diversification of Shariah-compliant products to compete with an increasingly aggressive conventional sector.

Dr Masrur Reaz, chairman of Policy Exchange Bangladesh, said the November performance signals a measured but meaningful recovery of the Islamic banking sector.

"The rebound in remittance inflows through Islamic banks is particularly significant, as remittances are fundamentally trust-based. This suggests that governance reforms and closer regulatory oversight are beginning to restore confidence among expatriate workers," he noted.

He observed that the double-digit growth in investments and assets reflects strong demand for Shariah-compliant financing, especially in rural and semi-urban areas where agent banking has emerged as a key strength.

"Islamic banks' dominance in agent banking underscores their comparative advantage in financial inclusion and grassroots deposit mobilisation," he added.Personal finance advice

However, Dr Reaz cautioned that sustaining this momentum would require deeper structural improvements.

"The sector must move beyond balance-sheet expansion and focus on risk management, product innovation, and greater transparency. Without diversification of Shariah-compliant instruments and stronger corporate governance, the gains may prove cyclical rather than structural," he said.

He also pointed out that the relatively weak performance in trade finance highlights the need for Islamic banks to enhance their capacity in export-import financing to remain competitive with conventional lenders.

SAJIBUR RAHMAN

Published :

Jan 25, 2026 08:22

Updated :

Jan 25, 2026 08:22

The Islamic banking sector in Bangladesh staged a significant comeback in November 2025, buoyed by a robust surge in inward remittances and a steady rise in Shariah-compliant investments.

After a period of structural adjustments and governance reforms, the sector recorded double-digit growth in investments and total assets, indicating a restoration of depositor confidence, particularly among expatriates and rural savers.

According to Bangladesh Bank (BB) data, the Islamic banking system recorded considerable growth in investments, rising 12.86 per cent to Tk 5.89 trillion in November 2025, up from Tk 5.21 trillion in the same month of the previous year.

While the conventional banking system also experienced growth -- rising from Tk 16.07 trillion to Tk 17.78 trillion -- its 10.60 per cent increase was slightly outpaced by Shariah-based lenders.

This expansion has solidified the Islamic sector's position, which now accounts for approximately one-fourth of total investment in the country's banking industry.

Total assets of Islamic banks saw a "robust growth" of 12.59 per cent, jumping from Tk 8.74 trillion to Tk 9.84 trillion during the period under review.

Perhaps the most striking highlight of the sector's performance is the recovery of its remittance share.

Remittances through Islamic channels surged from $472 million in November 2024 to $740 million in November 2025.

"The regained confidence of foreign workers in Islamic banks, likely due to improved management and tighter regulatory oversight, has been a primary driver for this 25.63 per cent jump in remittance share," said a senior central bank official.

In contrast, the trade sector showed more stability than growth.

Export proceeds via Islamic banks saw a slight decline of 4.41 per cent, standing at $668 million, while import payments marginally decreased 1.90 per cent to $1.04 billion.

Islamic banks continue to dominate the agent banking landscape, serving as a critical bridge for financial inclusion. Personal finance advice

They hold 54.58 per cent of total deposits in the agent banking arena. Deposits in this segment rose to Tk 261 billion in November 2025, marking a sharp 22.67 per cent year-on-year growth.

The BB report said full-fledged Islamic banks remain the primary drivers of the sector, sanctioning 91 per cent of all Islamic investments, while conventional banks operating through Islamic branches and windows contributed the remaining 9 per cent.

Industry experts suggest that while the sector has shown resilience, maintaining this momentum will require continued focus on governance and diversification of Shariah-compliant products to compete with an increasingly aggressive conventional sector.

Dr Masrur Reaz, chairman of Policy Exchange Bangladesh, said the November performance signals a measured but meaningful recovery of the Islamic banking sector.

"The rebound in remittance inflows through Islamic banks is particularly significant, as remittances are fundamentally trust-based. This suggests that governance reforms and closer regulatory oversight are beginning to restore confidence among expatriate workers," he noted.

He observed that the double-digit growth in investments and assets reflects strong demand for Shariah-compliant financing, especially in rural and semi-urban areas where agent banking has emerged as a key strength.

"Islamic banks' dominance in agent banking underscores their comparative advantage in financial inclusion and grassroots deposit mobilisation," he added.Personal finance advice

However, Dr Reaz cautioned that sustaining this momentum would require deeper structural improvements.

"The sector must move beyond balance-sheet expansion and focus on risk management, product innovation, and greater transparency. Without diversification of Shariah-compliant instruments and stronger corporate governance, the gains may prove cyclical rather than structural," he said.

He also pointed out that the relatively weak performance in trade finance highlights the need for Islamic banks to enhance their capacity in export-import financing to remain competitive with conventional lenders.