Bangladesh Defense

Bangladesh DefenseSaif

Senior Member

- Jan 24, 2024

- 20,444

- 9,566

- Nation

- Residence

- Axis Group

Govt's bank borrowing overshoots revised higher target in FY'26

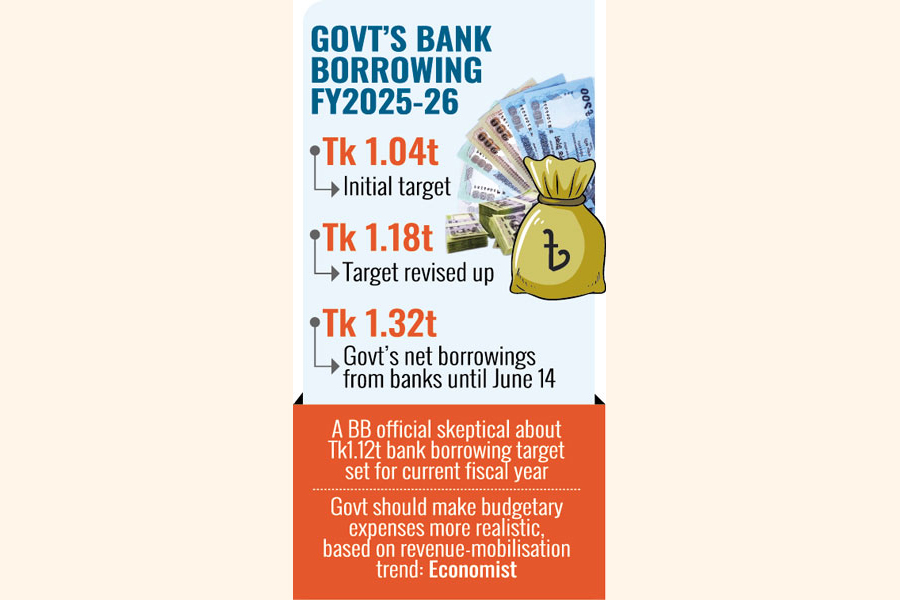

Government's bank-borrowing debt deepens as the borrowed aggregate sum ballooned over the revised higher target to Tk 1.32 trillion even before the just-past financial year's end. To meet budgetary shortfall, the government had initially set a bank-borrowing target of Tk 1.04 trillion for the fisc

Govt's bank borrowing overshoots revised higher target in FY'26

Jubair Hasan

Published :

Jul 03, 2026 00:09

Updated :

Jul 03, 2026 00:09

Government's bank-borrowing debt deepens as the borrowed aggregate sum ballooned over the revised higher target to Tk 1.32 trillion even before the just-past financial year's end.

To meet budgetary shortfall, the government had initially set a bank-borrowing target of Tk 1.04 trillion for the fiscal year 2025-2026 but less-than-expected level of revenue mobilisation prompted it to readjust the target upward to Tk 1.18 trillion in the middle of that fiscal.

But the growing credit appetite of the government because of poor revenue collection surpassed the target by a large margin even before the end of the fiscal year.

According to data with Bangladesh Bank (BB), the net government borrowings from the banking system until June 14 of the FY26 had amounted to around Tk 1.32 trillion, far outstripping the revised borrowing target set at Tk 1.18 trillion.

During this period, the government borrowed a net amount of Tk 1.23 trillion from the scheduled banks and Tk 83.09 billion from the central bank respectively, the data show.

The entire fiscal-yearend borrowing is expected to go up further as it was observed in the past that the government borrowing tendency normally goes up significantly in the last few weeks of a financial year.

Seeking anonymity, a BB official says the fund demand of the government continues to rise to meet its budgetary expenses because of lower revenue earnings.

He says the government bank borrowing keeps continuing to meet growing pressure of ADP (annual development programme) implementation by the last several weeks of the just-concluded fiscal year.

"I think the bank borrowing figure may cross Tk 1.40 trillion in FY'26 once the data are completed," the BB official told The Financial Express.

He further says the government very recently set the bank-borrowing target at Tk 1.12 trillion in this fiscal year (FY'27), which will be very difficult for them to maintain if the revenue collection is not increased significantly.

Responding to a question, the central banker says the demand for formal credits by the private sector is low while the commercial banks are very cautious in approving fresh loans to the entrepreneurs amid non-performing loan (NPL) buildups.

"Now, banks are increasingly perking their un-invested funds into government securities to make some gains during this economic slowdown. So, it is not causing crowding-out effect till now," the central banker adds.

According to the statistics of National Board of Revenue (NBR), the revenue authority managed to mobilise around Tk 4.20 trillion for the just-concluded fiscal year, shortening an anticipated large gap to Tk 800 billion against the revised budgetary target of Tk 5.03 trillion.

Chairman of Policy Exchange Bangladesh Dr M. Masrur Reaz says it is indicated that the fiscal consolidation is immediately needed, which is not happening.

He observes that the bank-borrowing projection has become extremely unpredictable because of the revenue collection which is also not predictable.

The economist says the commercial banks may get short-term benefits amid plummeting private-sector-credit growth. But the private-sector- credit demand is expected to increase in the coming days under this elected government.

"If it (private credit growth) happens and the current trend of government bank borrowing continues, it will definitely lead to crowding-out effect," he predicts.

Mr. Masrur was suggesting that the government should make the budgetary expenses more realistic, based on revenue-mobilisation trend, to avert such funding mismatch.

Jubair Hasan

Published :

Jul 03, 2026 00:09

Updated :

Jul 03, 2026 00:09

Government's bank-borrowing debt deepens as the borrowed aggregate sum ballooned over the revised higher target to Tk 1.32 trillion even before the just-past financial year's end.

To meet budgetary shortfall, the government had initially set a bank-borrowing target of Tk 1.04 trillion for the fiscal year 2025-2026 but less-than-expected level of revenue mobilisation prompted it to readjust the target upward to Tk 1.18 trillion in the middle of that fiscal.

But the growing credit appetite of the government because of poor revenue collection surpassed the target by a large margin even before the end of the fiscal year.

According to data with Bangladesh Bank (BB), the net government borrowings from the banking system until June 14 of the FY26 had amounted to around Tk 1.32 trillion, far outstripping the revised borrowing target set at Tk 1.18 trillion.

During this period, the government borrowed a net amount of Tk 1.23 trillion from the scheduled banks and Tk 83.09 billion from the central bank respectively, the data show.

The entire fiscal-yearend borrowing is expected to go up further as it was observed in the past that the government borrowing tendency normally goes up significantly in the last few weeks of a financial year.

Seeking anonymity, a BB official says the fund demand of the government continues to rise to meet its budgetary expenses because of lower revenue earnings.

He says the government bank borrowing keeps continuing to meet growing pressure of ADP (annual development programme) implementation by the last several weeks of the just-concluded fiscal year.

"I think the bank borrowing figure may cross Tk 1.40 trillion in FY'26 once the data are completed," the BB official told The Financial Express.

He further says the government very recently set the bank-borrowing target at Tk 1.12 trillion in this fiscal year (FY'27), which will be very difficult for them to maintain if the revenue collection is not increased significantly.

Responding to a question, the central banker says the demand for formal credits by the private sector is low while the commercial banks are very cautious in approving fresh loans to the entrepreneurs amid non-performing loan (NPL) buildups.

"Now, banks are increasingly perking their un-invested funds into government securities to make some gains during this economic slowdown. So, it is not causing crowding-out effect till now," the central banker adds.

According to the statistics of National Board of Revenue (NBR), the revenue authority managed to mobilise around Tk 4.20 trillion for the just-concluded fiscal year, shortening an anticipated large gap to Tk 800 billion against the revised budgetary target of Tk 5.03 trillion.

Chairman of Policy Exchange Bangladesh Dr M. Masrur Reaz says it is indicated that the fiscal consolidation is immediately needed, which is not happening.

He observes that the bank-borrowing projection has become extremely unpredictable because of the revenue collection which is also not predictable.

The economist says the commercial banks may get short-term benefits amid plummeting private-sector-credit growth. But the private-sector- credit demand is expected to increase in the coming days under this elected government.

"If it (private credit growth) happens and the current trend of government bank borrowing continues, it will definitely lead to crowding-out effect," he predicts.

Mr. Masrur was suggesting that the government should make the budgetary expenses more realistic, based on revenue-mobilisation trend, to avert such funding mismatch.