Bangladesh Defense

Bangladesh DefenseSaif

Senior Member

- Joined

- Jan 24, 2024

- Messages

- 16,488

- Likes

- 8,139

- Nation

- Residence

- Axis Group

New SME policy with no new strategies deplorable

THIS is unfortunate that the proposed National Small and Medium Enterprise Policy 2025 offers almost no new strategies to facilitate the growth of the sector. The proposal appears to echo the strategies of the 2019 policy that failed to help the sector grow. Such a repetition of failed...

www.newagebd.net

www.newagebd.net

New SME policy with no new strategies deplorable

15 January, 2025, 00:00

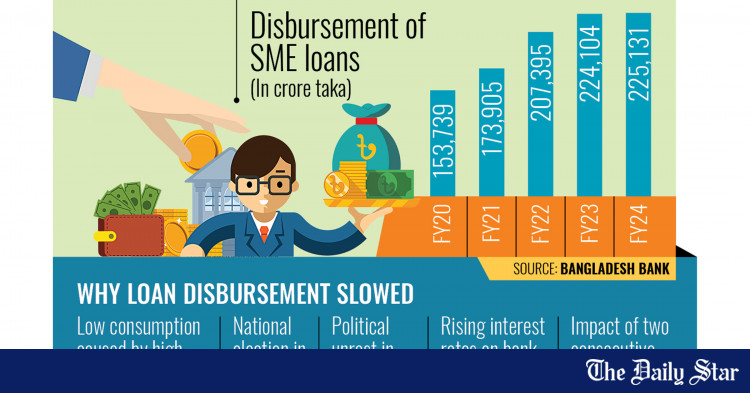

THIS is unfortunate that the proposed National Small and Medium Enterprise Policy 2025 offers almost no new strategies to facilitate the growth of the sector. The proposal appears to echo the strategies of the 2019 policy that failed to help the sector grow. Such a repetition of failed strategies reflects, as experts say, the government’s lack of commitment to addressing the systemic challenges that continue to hinder the growth of the medium enterprises. The policy proposal puts almost the same emphasis on the establishment of a 37-member SME council and recommends the continuation of a task force under the industries ministry. It also proposes 83 time-bound metrics, from the 63 metrics, to be implemented by ministries and divisions in 2025–2030 for the implementation of the policy. All this appears a mere bureaucratic expansion, devoid of any innovative solutions to the problems that small and medium entrepreneurs face. A lack of access to finance is one of the biggest obstacles to the growth of the sector, composed of about 7.8 million enterprises that employ about 80 per cent of workers in the informal sector. A World Bank report says that only 36 per cent of SMEs have access to formal credit, compared with 48 per cent in South Asia and 68 per cent in East Asia and Pacific.

Small entrepreneurs largely rely on loans from microfinance institutions at higher interest rates. Economists and policymakers have for long asked the authorities to ensure SME access to loans from banks and non-bank financial institutions and asked the regulatory authorities to cut the maximum interest rate in microfinance institutions, but to no avail. During the Covid-induced economic slowdown, financial institutions, as studies show, failed to disburse loans to them. Only 27 per cent of Tk 20,000 crore incentive announced by the Bangladesh Bank was disbursed. The proposed policy fails to offer any comprehensive solution to this issue. Instead, it simply iterates the need for an improved access to finance without offering clear, actionable strategies. The regulatory environment has also remained burdensome, further stymieing their growth. Issues such as complex tax structures, difficulties in trade licence renewals and the absence of one-stop services create unnecessary obstacles. The SME Foundation says that more than a half of SMEs blame complicated tax system and trade licence procedures as major hindrances. Entrepreneurs need to run to at least 34 departments to start a business. The proposed policy’s failure to address these systemic issues and continued reliance on failed strategies would leave SMEs with little hope to overcome challenges.

The government should, therefore, review the proposed policy with not only a new name but also with strategies. The policy should prioritise SME’s access to finance, simplify regulations, incentivise financial institutions for SME-friendly credit schemes and foster an ecosystem where SMEs can thrive.

15 January, 2025, 00:00

THIS is unfortunate that the proposed National Small and Medium Enterprise Policy 2025 offers almost no new strategies to facilitate the growth of the sector. The proposal appears to echo the strategies of the 2019 policy that failed to help the sector grow. Such a repetition of failed strategies reflects, as experts say, the government’s lack of commitment to addressing the systemic challenges that continue to hinder the growth of the medium enterprises. The policy proposal puts almost the same emphasis on the establishment of a 37-member SME council and recommends the continuation of a task force under the industries ministry. It also proposes 83 time-bound metrics, from the 63 metrics, to be implemented by ministries and divisions in 2025–2030 for the implementation of the policy. All this appears a mere bureaucratic expansion, devoid of any innovative solutions to the problems that small and medium entrepreneurs face. A lack of access to finance is one of the biggest obstacles to the growth of the sector, composed of about 7.8 million enterprises that employ about 80 per cent of workers in the informal sector. A World Bank report says that only 36 per cent of SMEs have access to formal credit, compared with 48 per cent in South Asia and 68 per cent in East Asia and Pacific.

Small entrepreneurs largely rely on loans from microfinance institutions at higher interest rates. Economists and policymakers have for long asked the authorities to ensure SME access to loans from banks and non-bank financial institutions and asked the regulatory authorities to cut the maximum interest rate in microfinance institutions, but to no avail. During the Covid-induced economic slowdown, financial institutions, as studies show, failed to disburse loans to them. Only 27 per cent of Tk 20,000 crore incentive announced by the Bangladesh Bank was disbursed. The proposed policy fails to offer any comprehensive solution to this issue. Instead, it simply iterates the need for an improved access to finance without offering clear, actionable strategies. The regulatory environment has also remained burdensome, further stymieing their growth. Issues such as complex tax structures, difficulties in trade licence renewals and the absence of one-stop services create unnecessary obstacles. The SME Foundation says that more than a half of SMEs blame complicated tax system and trade licence procedures as major hindrances. Entrepreneurs need to run to at least 34 departments to start a business. The proposed policy’s failure to address these systemic issues and continued reliance on failed strategies would leave SMEs with little hope to overcome challenges.

The government should, therefore, review the proposed policy with not only a new name but also with strategies. The policy should prioritise SME’s access to finance, simplify regulations, incentivise financial institutions for SME-friendly credit schemes and foster an ecosystem where SMEs can thrive.