Bangladesh Defense

Bangladesh DefenseSaif

Senior Member

- Jan 24, 2024

- 20,536

- 9,606

- Nation

- Residence

- Axis Group

Inflation rises to 8.49% in December

Following months of a brief pause, inflationary pressures continued to rise in December for the second consecutive month.

Inflation rises to 8.49% in December

Following months of a brief pause, inflationary pressures continued to rise in December for the second consecutive month.

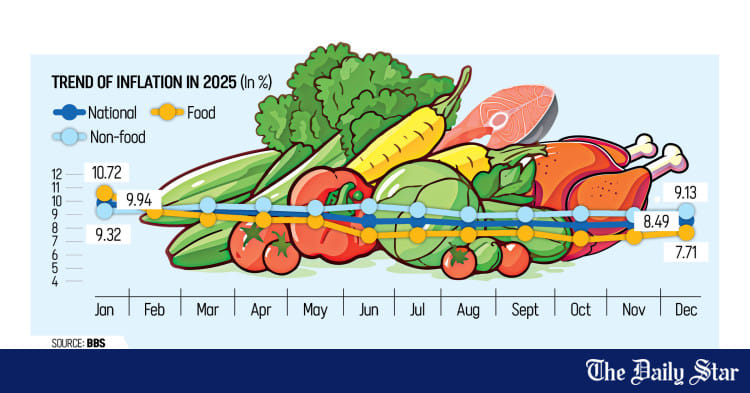

Headline inflation reached 8.49 percent in the last month of the year, up from 8.29 percent in November and October's 39-month low of 8.17 percent, according to data released by the Bangladesh Bureau of Statistics (BBS) yesterday.

For low and fixed-income households in both rural and urban areas, the latest increase adds fresh pressure on the cost of food and non-food essentials.

Economists say inflation is turning red-hot again despite the central bank's tightened monetary stance, pointing to supply-side constraints rather than rising demand as the main driver of price increases.

While this view questions the effectiveness of the current high policy rate and calls for closer market monitoring, economists still support keeping lending rates elevated.

In December, food inflation climbed to 7.71 percent from 7.36 percent in November, adding pressure on household budgets as prices of essential items edged up.

Non-food inflation also increased slightly to 9.13 percent from 9.08 percent a month earlier.

BBS data showed that the consumer price index (CPI), which tracks changes in the cost of a basket of goods and services, rose in both rural and urban areas.

According to the Trading Corporation of Bangladesh (TCB), prices of essential food items such as rice, flour, edible oil and lentils were higher in December compared to the same month last year.

Bangladesh has been facing persistent inflation for nearly three years. Consumer prices remained above 9 percent until May 2025 and have stayed above 8 percent since then, raising questions about the effectiveness of recent economic policies.

However, in index terms, food inflation showed a slight easing in December. The food CPI declined to 142.88 in December from 146.66 in November, although it increased on a year-on-year basis, BBS data showed.

"Inflation remains very high, and the data show no clear sign of a lasting decline," said Zahid Hussain, former lead economist of the World Bank Dhaka office.

"The measures taken so far to control inflation have not produced visible results. The current tightening measures are still not strong enough to bring prices down," he added.

Hussain also said food inflation in Bangladesh is not driven by exchange rates or credit conditions. "Instead, it largely follows its own past trend. This means structural and supply-side factors mainly drive food inflation, and demand-side measures alone are unlikely to work," he said.

He added that the data suggest it is too early to ease policy and questioned whether the current level of tightening is sufficient to achieve the intended outcome.

Sharing a similar view, Mustafa K Mujeri, executive director of the Institute for Inclusive Finance and Development (InM), questioned the effectiveness of the existing tightening monetary policy.

"If the policies adopted so far were working, inflation should have come down by now. Instead, inflation has stayed above 8 percent for several months, raising doubts about the effectiveness of the existing measures," he said.

He added that Bangladesh has followed a contractionary monetary policy for a long period, but it has failed to deliver the expected results because inflation is not driven by demand alone.

Mujeri said supply-side weaknesses, particularly poor market management and problems in the value chain, continue to keep inflation high, allowing powerful intermediaries to create artificial shortages and push up prices.

He added that higher prices often do not benefit producers such as farmers, as most of the gains go to intermediaries.

Without stronger market oversight and a coordinated approach involving monetary, fiscal, supply-side and credit policies, contractionary monetary policy alone cannot reduce inflation in a country like Bangladesh, Mujeri said.

Following months of a brief pause, inflationary pressures continued to rise in December for the second consecutive month.

Headline inflation reached 8.49 percent in the last month of the year, up from 8.29 percent in November and October's 39-month low of 8.17 percent, according to data released by the Bangladesh Bureau of Statistics (BBS) yesterday.

For low and fixed-income households in both rural and urban areas, the latest increase adds fresh pressure on the cost of food and non-food essentials.

Economists say inflation is turning red-hot again despite the central bank's tightened monetary stance, pointing to supply-side constraints rather than rising demand as the main driver of price increases.

While this view questions the effectiveness of the current high policy rate and calls for closer market monitoring, economists still support keeping lending rates elevated.

In December, food inflation climbed to 7.71 percent from 7.36 percent in November, adding pressure on household budgets as prices of essential items edged up.

Non-food inflation also increased slightly to 9.13 percent from 9.08 percent a month earlier.

BBS data showed that the consumer price index (CPI), which tracks changes in the cost of a basket of goods and services, rose in both rural and urban areas.

According to the Trading Corporation of Bangladesh (TCB), prices of essential food items such as rice, flour, edible oil and lentils were higher in December compared to the same month last year.

Bangladesh has been facing persistent inflation for nearly three years. Consumer prices remained above 9 percent until May 2025 and have stayed above 8 percent since then, raising questions about the effectiveness of recent economic policies.

However, in index terms, food inflation showed a slight easing in December. The food CPI declined to 142.88 in December from 146.66 in November, although it increased on a year-on-year basis, BBS data showed.

"Inflation remains very high, and the data show no clear sign of a lasting decline," said Zahid Hussain, former lead economist of the World Bank Dhaka office.

"The measures taken so far to control inflation have not produced visible results. The current tightening measures are still not strong enough to bring prices down," he added.

Hussain also said food inflation in Bangladesh is not driven by exchange rates or credit conditions. "Instead, it largely follows its own past trend. This means structural and supply-side factors mainly drive food inflation, and demand-side measures alone are unlikely to work," he said.

He added that the data suggest it is too early to ease policy and questioned whether the current level of tightening is sufficient to achieve the intended outcome.

Sharing a similar view, Mustafa K Mujeri, executive director of the Institute for Inclusive Finance and Development (InM), questioned the effectiveness of the existing tightening monetary policy.

"If the policies adopted so far were working, inflation should have come down by now. Instead, inflation has stayed above 8 percent for several months, raising doubts about the effectiveness of the existing measures," he said.

He added that Bangladesh has followed a contractionary monetary policy for a long period, but it has failed to deliver the expected results because inflation is not driven by demand alone.

Mujeri said supply-side weaknesses, particularly poor market management and problems in the value chain, continue to keep inflation high, allowing powerful intermediaries to create artificial shortages and push up prices.

He added that higher prices often do not benefit producers such as farmers, as most of the gains go to intermediaries.

Without stronger market oversight and a coordinated approach involving monetary, fiscal, supply-side and credit policies, contractionary monetary policy alone cannot reduce inflation in a country like Bangladesh, Mujeri said.